Certificate form 2 personal income tax sample. Nuances of filling out the form

What form should I use to generate the 2-NDFL certificate for 2016? Has the new certificate form been approved? How long does it take to submit a certificate for 2016 to the Federal Tax Service? How to reflect new income and deduction codes in the certificate? You will find answers to these and other questions in this article, and you can also familiarize yourself with a sample of filling out a 2-NDFL certificate for 2016.

Who must submit 2-NDFL for 2016

Organizations and individual entrepreneurs that are recognized as tax agents for personal income tax must withhold and transfer to the personal income tax budget from income paid to individuals. In addition, tax agents are required to report this to the Federal Tax Service at the end of each year. For these purposes, 2-NDFL certificates are annually submitted to the tax inspectorates.

When you can not submit 2-NDFL

There is no need to submit 2-NDFL certificates in 2017 if during 2016 the organization or individual entrepreneur did not pay income to individuals for which they are tax agents. So, for example, you don’t have to report on employees for whom the organization did not pay wages or make any other payments from January to December 2016. There is no need to submit 2-NDFL with zero indicators. There is simply no point in zero 2-NDFL certificates.

Deadline

Organizations and individual entrepreneurs are required to submit 2-NDFL certificates about income and withheld personal income tax to the Federal Tax Service no later than April 1 of the year following the reporting year (clause 2 of Article 230 of the Tax Code of the Russian Federation). However, April 1, 2017 is a Saturday. In this regard, the deadline for submission is moved to the next working day. Accordingly, most tax agents need to submit 2-NDFL certificates for 2016 with “sign 1” no later than April 3, 2017 (inclusive).

Also, information must be submitted to the Federal Tax Service Inspectorate in Form 2-NDFL in relation to individuals to whom the tax agent paid income in 2016, but personal income tax was not withheld from this income. For example, if in 2016 an organization gave a gift worth more than 4,000 rubles to a citizen who is not its employee. The deadline for submitting such certificates is no later than March 1 of the year following the reporting year (clause 5 of Article 226 of the Tax Code of the Russian Federation). Accordingly, if you paid income to individuals in 2016 from which personal income tax was not withheld, then no later than March 1, 2017 (this is Monday) you need to submit 2-NDFL certificates to the Federal Tax Service Inspectorate for these individuals with the “2” order. Moreover, within the same period, the “physicist” himself must be notified about the unwithheld tax. Cm. " ".

Presentation method

It is possible to submit 2-NDFL certificates “on paper” only if in 2016 the number of individuals who received income from a tax agent is less than 25 people (Clause 2 of Article 230 of the Tax Code of the Russian Federation). If 25 or more people received income, then they must report electronically via telecommunications channels through an electronic document management operator.

New form: approved or not

The form of a certificate of income for an individual 2-NDFL and the procedure for filling it out were approved by order of the Federal Tax Service of Russia dated October 30, 2015 No. ММВ-7-11/485. At the same time, a new form of 2-NDFL certificate for reporting for 2016 was not developed or approved. The new form simply does not exist. In 2017, you need to fill out the form that was used before when reporting for 2015 was submitted. Cm. " ".

![]()

The composition of the current form of certificate 2-NDFL is as follows:

You can download the current 2-NDFL certificate form here.

Filling out the certificate: useful samples

Formatting the title

In the title of the certificate for 2016, in the “attribute” field, mark 1 if the certificate is provided as an annual report on income and withheld amounts of income tax (clause 2 of Article 230 of the Tax Code of the Russian Federation). If you simply inform the Federal Tax Service that in 2016 it was impossible to withhold tax, then indicate the number “2” (clause 5 of Article 226 of the Tax Code of the Russian Federation).

In the “Adjustment number” field, show one of the following codes:

- 00 – when preparing the initial certificate;

- 01, 02, 03, etc. – if you fill out a corrective certificate (that is, if in 2017 you “correct” previously submitted information”);

- 99 – when filling out a cancellation certificate (when you need to completely “cancel” the information already submitted before).

In the “In the Federal Tax Service (code)” field, mark the tax office code, indicate the year “2016” in the title, and also assign a serial number and date of generation to the certificate. As a result, the title of the 2-NDFL certificate for 2016 may take the following form:

Section 1: enter information about the tax agent

In section 1 of the form, provide basic information about the organization: name, tax identification number, checkpoint, contact telephone number. However, keep in mind that individual entrepreneurs indicate only the TIN, and they put a dash in the checkpoint field.

If income to an individual was paid by the head office of the company in 2016, then in the 2-NDFL certificate you need to show the TIN, KPP and OKTMO at the location of the head office. If the income was received from a separate division, then mark the checkpoint and OKTMO at the location of the “separate division”.

In the “OKTMO Code” field, indicate the code of the territory in which the tax agent is registered. You can recognize this code by the Classifier approved by order of Rosstandart dated June 14, 2013 No. 159-st. However, if the 2-NDFL certificate is generated on behalf of an individual entrepreneur, then the approach when filling out should be as follows:

- indicate OKTMO at the place of residence of the entrepreneur according to the passport (except for individual entrepreneurs on UTII and on the patent taxation system);

- if the individual entrepreneur is on “imputed” or “patent”, then reflect OKTMO at the place of business in the appropriate tax regime.

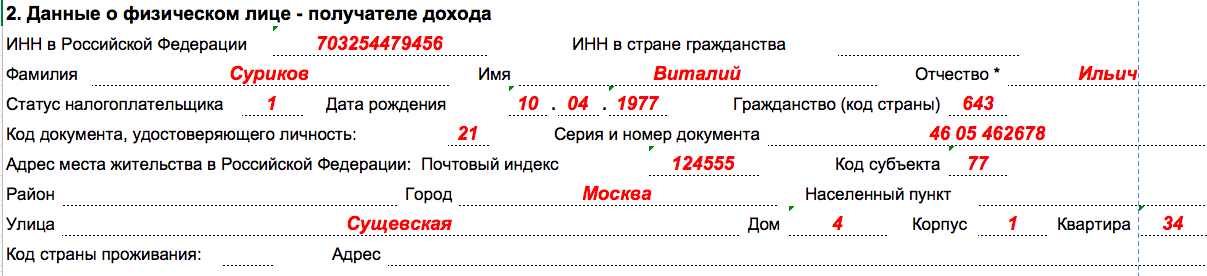

Section 2: fill in information about the recipient

In section 2, enter the details of the individual to whom the income was paid. So, in particular, indicate your full name and tax identification number, date of birth. We will explain in more detail how to fill out section 2 of the 2-NDFL certificate for 2016 in the table:

| Filling out the fields in section 2 of the 2-NDFL certificate | |

|---|---|

| Field | What to indicate |

| "TIN in the Russian Federation" | Identifier specified in the TIN certificate of an individual. |

| "TIN in the country of residence" | TIN or its equivalent in the country of citizenship of the foreign employee. |

| "Taxpayer status" | One of the following codes: 1 – for tax residents; 2 – for non-residents (including for citizens of the EAEU: the Republic of Belarus, Kazakhstan, Armenia and Kyrgyzstan); 3 – for non-residents – highly qualified specialists; 4 – for employees who are participants in the state program for the voluntary resettlement of compatriots living abroad; 5 – for foreign employees who have refugee status or have received temporary asylum in the Russian Federation; 6 – for foreign employees working on the basis of a patent. |

| "Citizenship (country code)" | Code of the country of permanent residence of the person. The code, for example, of Russia is 643 (according to the Classifier, approved by Resolution of the State Standard of Russia dated December 14, 2001 No. 529-st). |

| “Identity document code” | Code from the reference book “Document Codes” (Appendix 1 to the order of the Federal Tax Service of Russia dated October 30, 2015 No. ММВ-7-11/485). |

| “Residence address in the Russian Federation” | Address of permanent residence of an individual according to a passport or other document confirming such address. |

| Subject code | Directory code “Codes of subjects of the Russian Federation and other territories (Appendix 2 to the order of the Federal Tax Service of Russia dated October 30, 2015 No. ММВ-7-11/485). |

Section 3: grouping income

In the table of section 3 of the 2-NDFL certificate for 2016, show the amount of income received for 2016, the codes of income and deductions and the tax rate. Please fill out this table monthly. At the beginning of the table, show the tax rate at which the income reflected in this section is taxed. If in 2016 an individual was paid income taxed with personal income tax at different rates, then fill out section 3 several times - at each rate.

Let us remind novice accountants that each type of income and each type of tax deductions are assigned individual codes, for example:

- for income in the form of wages - code 2000;

- when paying remuneration under other civil contracts (except copyright) – code 2010;

- when paying benefits for temporary disability - code 2300;

- if there is no separate code for income - code 4800. That is, for example, under code 4800 you can show above-limit daily allowances, compensation for unused vacation, severance pay in excess of three times the average earnings, etc. (letter of the Federal Tax Service of Russia dated September 19, 2016 No. BS- 4-11/17537).

If we talk about the most common case, then if an employee in the period from January to December 2016 received only wages under an employment contract, then section 3 of the 2-NDFL certificate for 2016 with sign “1” may look like this:

Also, in section 3 of the 2-NDFL certificate for 2016, you need to reflect the codes of deductions provided to individuals and the amount of such deductions. However, do not get confused: in section 3, reflect only professional tax deductions (Article 221 of the Tax Code of the Russian Federation), deductions in the amounts provided for in Article 217 of the Tax Code of the Russian Federation and amounts that reduce the tax base on the basis of Articles 214.1, 214.3, 214.4 of the Tax Code of the Russian Federation. The corresponding deduction code must be indicated opposite the income for which this deduction is applied.

New income codes from 2017

In 2-NDFL certificates, separately show the bonuses that employees received in 2016 for production results as part of their remuneration. For such bonuses, code 2002 has been in effect since 2017. If bonuses were issued at the expense of net profit, then show them with code 2003. Note that until 2017, bonuses were not allocated with a separate code: for bonuses for labor, the same code was indicated as for salary in cash – 2000.

Standard, social, investment and property tax deductions should not be reflected in section 3 of 2-NDFL certificates. The following section of the 2-NDFL certificate is provided for them.

Section 4: highlighting deductions

In section 4 of the 2-NDFL certificate, show the standard tax deductions provided in 2016 (Article 218 of the Tax Code of the Russian Federation), social (Article 219 of the Tax Code of the Russian Federation), investment, and property deductions for the purchase (construction) of housing (subparagraph 2, paragraph. 1 Article 220 of the Tax Code of the Russian Federation). The code that must be entered in the “Deduction Code” column can be determined from Appendix 2 to the order of the Federal Tax Service of Russia dated September 10, 2015 No. ММВ-7-11/387. In the “Deduction Amount” column, enter the deduction amount corresponding to the specified code.

Some social and property deductions are provided by employers to their employees. In this regard, in the lines “Notification confirming the right to a social tax deduction” and “Notification confirming the right to a property tax deduction,” the accountant needs to note the number and date of the corresponding notification and the code of the Federal Tax Service that issued the notification.

Changes in deduction codes since 2017

You can also find a complete list of income and deduction codes that may be required to generate a 2-NDFL certificate for 2016 in the material: "".

Let's assume that an employee was provided with a standard tax deduction for their first child in 2016. In 2017, this deduction corresponds to deduction code 126. The deduction amount was 16,800 rubles. In this case, an example of filling out section 4 of the 2-NDFL certificate for 2016 will look like this:

Show all figures in the certificate for 2016 (except for the personal income tax amount) in rubles and kopecks. However, reflect the amount of tax (personal income tax) in full rubles (do not take into account amounts up to 50 kopecks, amounts of 50 kopecks or more - round up to the nearest whole ruble). For example, if the tax is 15.78 rubles, then show 16 whole rubles on the certificate.

Section 5: summing up

In section 5 of the certificate, summarize the total amount of income of an individual and personal income tax at the end of 2016 for each tax rate. If, during the tax period, the tax agent paid an individual income taxed at different rates (for example, 9%, 13%, 15%, 30%, 35%), then for each of them it is necessary to create sections 3 - 5 of certificate 2 -NDFL. Below in the table we will explain the general procedure for filling out the 2-NDFL certificate for 2016.

| General procedure for filling out the 2-NDFL certificate for 2016 | ||

|---|---|---|

| Help field | Filling | |

| 2-NDFL with sign 1 | 2-NDFL with sign 2 | |

| "Total Income" | Total income at the end of 2016 (excluding deductions). | The total amount of income in 2016 from which personal income tax was not withheld. |

| "The tax base" | The tax base from which personal income tax was calculated in 2016. | Tax base for calculating personal income tax |

| "Tax amount calculated" | The amount of calculated personal income tax (the tax base is multiplied by the tax rate). | The amount of personal income tax that has been calculated but not withheld. |

| “Amount of fixed advance payments” | The amount of fixed advance payments by which the personal income tax should be reduced (data taken from the notification of the Federal Tax Service). | 0 |

| "Tax amount withheld" | The amount of personal income tax withheld from the income of an individual. | 0 |

| “Tax amount transferred” | The amount of personal income tax transferred for 2016. | 0 |

| “Amount of tax over-withheld by the tax agent” | The over-withheld amount of personal income tax not returned by the tax agent, as well as the amount of overpayment of personal income tax due to a change in tax status. | 0 |

| “The amount of tax not withheld by the tax agent” | The calculated amount of personal income tax not withheld in 2016. | |

Here is an example of filling out section 5 of the 2-NDFL certificate for 2016. Let's assume that the income of an individual for 2017 was 549,200 rubles. After applying tax deductions, the tax base amounted to 457,500 rubles. The tax rate is 13 percent. This means the personal income tax amount is 59,475 rubles (457,500 x 13%). This amount was calculated and withheld by the employer at the end of 2016. And I filled out section 5 of the help like this:

As a result, after filling out all the above sections, a sample 2-NDFL certificate for 2016 with sign “1” may look like this:

Responsibility of tax agents

If you do not submit a certificate in form 2-NDFL for 2016 to the Federal Tax Service on time, the tax authorities will have the right to impose a fine on the organization or individual entrepreneur under Article 126 of the Tax Code of the Russian Federation: 200 rubles.

Also, for failure to submit or for late submission of the annual 2-NDFL certificate, at the request of the Federal Tax Service, the court may impose administrative liability in the form of a fine in the amount against the manager or chief accountant: from 300 to 500 rubles. (Article 15.6 of the Code of Administrative Offenses of the Russian Federation).

In addition, if inspectors from the Federal Tax Service identify errors in 2-NDFL, they may regard them as “unreliable information.” And then the tax agent can be additionally fined 500 rubles for each “unreliable” document. If there are a lot of erroneous certificates, then the fine may increase.

Probably more than half of all employed citizens sooner or later faced the need to obtain documentation of their income. This function is performed by the 2-NDFL certificate, which contains all the information about the taxpayer for the period specified in it. With the development of information technology, people are increasingly interested in the question of how to obtain a 2-NDFL tax certificate online. And is it possible to print it and download it through your personal account on the website of the tax service or the government services portal, how to do this and where to go. The Federal Tax Service recently posted up-to-date information on this matter on its website.

What is a 2-NDFL certificate?

The abbreviation NDFL stands for personal income tax. This includes any income and profit, regardless of the source of their receipt - work in a budgetary organization, with an individual entrepreneur, etc.

Certificate 2-NDFL was developed in a special way to indicate all relevant information about the taxpayer. Visually, the document includes the following blocks of information:

- “header” – indicates the code of the territorial tax authority;

- information block is the taxpayer’s financial data for a specific time interval (profit received, tax paid, deductions);

- details of the responsible person - signature of the accountant/manager and stamp of the organization (optional).

The document in question is issued by a tax agent, represented by the employer. Such a certificate is usually necessary for obtaining a loan, submitting information to judicial authorities, when applying for a visa and many other situations.

Is it possible to do 2-NDFL online: history of the issue

In 2014, a message appeared on the Federal Tax Service website, which talked about obtaining data on the 2-NDFL certificate online (here is the exact link - https://www.nalog.ru/rn53/news/activities_fts/4645858/). Then most users read the information inattentively or saw what they wanted to see. Namely, the ability to download and print 2-NDFL online in your personal account.

In fact, payers were provided only with information about the submitted certificate as an obligation of the tax agent (information about income, deductions, etc.). It was not possible to download this document, nor was it possible to use its electronic version instead of paper.

This news was discussed on many forums for a long time and even options for downloading help were invented. For example, some users gave “instructions” on how to obtain 2-personal income tax online through their personal account. To do this, it was suggested to move the mouse cursor over the “print version” icon and download the document in PDF format. Or simply take a screenshot of the help screen and print it on a printer. But all these efforts were in vain for one simple reason - the printed file could not have legal force without the original signature of the tax agent.

You can get it online!

Since November 2017, each owner of a personal account on the official website of the Federal Tax Service of Russia has a real opportunity to obtain a 2-NDFL certificate online. Of course, provided that the relevant employer submitted it to the tax office.

The document can now not only be viewed, but also downloaded + saved to your computer for later printing.

Available file formats are pdf and xml. In addition, the individual’s income certificate will be signed with an enhanced qualified electronic signature of the Federal Tax Service.

Since it is now possible to obtain a legal and official income certificate online, the main advantage is that you no longer need to go to the accounting department at your place of work (current or past) to obtain a 2-NDFL certificate about your income.

In addition, the innovation makes it possible to immediately send a 2-NDFL certificate in electronic form. For example, to a bank.

Please note that some users and even websites claim that it is possible to obtain a certificate through the government service portal https://www.gosuslugi.ru. In fact, this is impossible. This site does not provide information about taxes to its users, but instead provides only a link to the website of the Federal Tax Service of Russia.

Thus, gone are the days when 2-NDFL was issued only by the employer and only in paper form.

The service allows you to:

- Prepare a report

- Generate file

- Test for errors

- Print report

- Send via Internet!

2-NDFL certificates in 2018: new form and sample filling

The form of the 2-NDFL certificate and the procedure for filling it out were approved by order of the Federal Tax Service of Russia dated October 30, 2015 No. ММВ-7-11/485@ (as amended by the order of the Federal Tax Service of Russia dated January 17, 2018 No. ММВ-7-11/19@). It is valid throughout 2018. From January 1, 2019, a new certificate will be applied. It was approved by order of the Federal Tax Service of Russia dated October 2, 2018 No. ММВ-7-11/566@.

Changes in the new form:

- drawn up on machine-readable form;

- for employees and for the Federal Tax Service is formed on different forms.

Who must prepare and submit 2-NDFL certificates

Certificates in form 2-NDFL must be submitted by organizations and individual entrepreneurs that pay income to individuals. This obligation is enshrined in clause 1, clause 2 of Art. 226 and paragraph 2 of Art. 230 Tax Code of the Russian Federation.

There is no need to submit 2-NDFL certificates if you paid to an individual:

Only non-taxable income (clause 28 of Article 217 of the Tax Code of the Russian Federation, letter of the Federal Tax Service of Russia dated January 19, 2017 No. BS-4-11/787@);

Income on which an individual must pay tax and submit a declaration (Article 227, Article 228 of the Tax Code of the Russian Federation);

Income specified in Art. 226.1 Tax Code of the Russian Federation.

If in the reporting (expired) year the organization did not pay an individual income from which personal income tax was required to be withheld, then a 2-NDFL (“zero”) certificate does not need to be submitted. For example, if you paid only non-taxable income specified in Art. 217 Tax Code of the Russian Federation.

Where to submit 2-NDFL

In accordance with paragraph 2 of Art. 230 of the Tax Code of the Russian Federation, tax agents submit reporting on 2-NDFL to the tax authority at the place of their registration.

Submit 2-NDFL for employees of separate departments to the Federal Tax Service at the place of their registration. The same thing happens when a separate division pays income to individuals according to the GPA.

What income should be included in the 2-NDFL certificate 2018

How to fill out a 2-NDFL certificate

The general requirements for filling out the 2-NDFL certificate are as follows:

- 2-NDFL certificates are filled out by the tax agent based on the data contained in the tax registers.

- If the tax agent accrued income to an individual during the tax period that is taxed at different tax rates, sections 3-5 are completed for each rate.

- When filling out the Certificate form, codes for the types of income of the taxpayer, codes for the types of deductions of the taxpayer, the Directories “Codes of types of documents proving the identity of the taxpayer” (Appendix 1 of the Procedure for filling out the certificate) and “Codes of the subjects of the Russian Federation and other territories” (Appendix 2 of the Procedure for filling out the certificate) are used.

- All details and totals are filled in in the Certificate form. If there is no value for the total indicators, zero is indicated.

- Certificates in electronic form are generated in accordance with the format (xml) for submitting information on the income of individuals in form 2-NDFL.

Table 2. How to fill out 2-NDFL certificates

|

Chapter |

Information to be provided |

|

Heading |

Indicated: Tax period for which the Certificate form is prepared; Serial number of the Certificate in the reporting tax period; Date of preparation of the form; The “Sign” is indicated and the following is entered: number 1 - if Certificate 2-NDFL is submitted based on the provisions of clause 2 of Art. 230 Tax Code of the Russian Federation; number 2 - if the Certificate is submitted in accordance with the provisions of clause 5 of Art. 226 Tax Code of the Russian Federation. When drawing up the initial form of the Certificate, “00” is entered in the “Adjustment number” field; When drawing up a corrective Certificate to replace the previously submitted one, a value one more than that indicated in the previous Certificate is indicated (For example, “01”, “02”, etc.); When drawing up a canceling Certificate, the number “99” is entered instead of the previously submitted one. In the field “in the Federal Tax Service (code)” - the four-digit code of the tax authority with which the tax agent is registered. (Section II of the Procedure for filling out the certificate) |

|

Section 1 “Data about the tax agent” |

The OKTMO code and contact telephone number of the tax agent are indicated; TIN and checkpoint; name of the organization according to its constituent documents (Section III of the Procedure for filling out the certificate) |

|

Section 2 “Data about the individual - recipient of income” |

The TIN of the individual taxpayer is indicated; last name, first name and patronymic of the individual - taxpayer; taxpayer status code; Date of Birth; numeric code of the country of which the taxpayer is a citizen; code of the type of identification document and its details; full address of the taxpayer's place of residence; (Section IV of the Procedure for filling out the certificate) |

|

Section 3 “Income taxed at the rate of __%” |

information on income accrued and actually received by an individual in cash and in kind, as well as in the form of material benefits, by month of the tax period and corresponding deductions is indicated. (Section V of the Procedure for filling out the certificate) |

|

Section 4 “Standard, social, investment and property tax deductions” |

information about standard, social, investment and property tax deductions provided by the tax agent is reflected. (Section VI of the Procedure for filling out the certificate) |

|

Section 5 “Total amounts of income and tax” |

the total amounts of accrued and actually received income, calculated, withheld and transferred personal income tax are reflected at the appropriate rate specified in the title of Section 3. (Section VII of the Procedure for filling out the certificate) |

How to fill out 2-NDFL in an accounting program

Let's consider the procedure for filling out certificates in accounting programs: Bukhsoft Online, 1C: Accounting and Kontur.Accounting.

Bukhsoft Online

1. Go to the “ ” module in the Funds/NDFL section and select “2-NDFL”.

2. In the window that opens, in the “Questionnaire” tab, fill out and check the employee’s information.

4. In the window that opens, reflect the data for sections 3-5 of the 2-NDFL certificate.

1C:Enterprise

1. Go to the section “Salaries and personnel/NDFL/2-NDFL for transfer to the Federal Tax Service”. Click "Create".

2. Fill out the header and signatures.

3. Then, using the “Fill” button, start the procedure for automatically collecting information about the income of individuals according to the information base. The list of prepared certificates of income of individuals will be displayed in the tabular part of the document. When automatically filled out, the document includes only those amounts of income, deductions and taxes of individuals that relate to the OKTMO/KPP specified in the header of the document. If necessary, the data in the employee’s 2-NDFL document can be corrected manually, but instead it is recommended to correct the credentials themselves, and then refill the data in the document.

4. The data on the “Personal Data” tab is filled in automatically. If some personal data is not filled in or filled in incorrectly, you can directly change the employee’s personal data from the document form using the “Edit employee card” link. The edited data will be updated in the form automatically.

The details of the notification for tax reduction on advance payments (number, date of notification and code of the Federal Tax Service that issued it) are filled in automatically with the data specified in the document “Advance payment for personal income tax”.

5. After preparing the information, the document “2-NDFL for transfer to the Federal Tax Service” should be written down.

Kontur.Accounting

1. In the main program window, select the “Reporting” tab and click the “Create report” button.

2. In the window that opens, in the “Federal Tax” section, select the “2-NDFL” item. And indicate the reporting period.

2-NDFL for the year from 01/01/2019 may look different depending on who you are preparing it for: for the tax office or for the employee. How to correctly issue a 2-NDFL certificate for the Federal Tax Service? What nuances should be taken into account when preparing a certificate for an employee? When should the form be submitted to the fiscal authorities? What happens if you refuse to issue an employee a 2-NDFL certificate? In the article we will consider these and other questions, and also provide a sample of filling out the form for the Federal Tax Service.

General information about the document: purpose and due date

Certificate 2-NDFL is needed to inform the Federal Tax Service and taxpayers about payments, subject to personal income tax, transferred by tax agents in favor of individuals:

- workers;

- contractors;

- recipients of dividends.

A separate 2-NDFL certificate is issued for each recipient of payments. Therefore, if a certificate for any employee is not submitted, a fine of 200 rubles will be imposed on the tax agent. (clause 1 of article 126 of the Tax Code of the Russian Federation). In addition, if false data is found in any certificate, the Federal Tax Service has the right to fine him 500 rubles. (Article 126.1 of the Tax Code of the Russian Federation). If the company has a large staff and massive failure to submit certificates or submit certificates with errors, the financial blow to the business caused by the sanctions of the Federal Tax Service can be noticeable.

The new form of certificate 2-NDFL was approved by order of the Federal Tax Service dated October 2, 2018 No. ММВ-7-11/566@. Starting from the reporting campaign for 2018, the form should be drawn up on this updated form, which comes into effect from 01/01/2019. An important nuance: there are now two forms - one for information submitted to the tax office, the second - for a certificate issued to an individual.

You can familiarize yourself with the changes to 2-NDFL.

There are two types of certificates to be submitted to the Federal Tax Service:

1. As certificates reflecting all income, regardless of whether personal income tax is withheld from them or not. The certificate indicates sign 1.

2. As certificates separately reflecting those incomes for which personal income tax is not withheld. The certificate indicates sign 2.

A sample of filling out the 2-NDFL certificate for the Federal Tax Service can be downloaded from the link below.

Thus, the potential for penalties to arise doubles.

You can find out more about the relevant penalties from this article .

Let's study in more detail the main nuances of using the document, as well as how to correctly fill out 2-NDFL for the year.

Issuing a certificate at the request of an individual: nuances

The tax agent is obliged to urgently generate a 2-NDFL certificate at the request of the recipient of income paid by the agent (clause 3 of Article 230 of the Tax Code of the Russian Federation). The document must be issued to the person within 3 days after receiving a written request from him and necessarily upon dismissal (Article 62, 84.1 of the Labor Code of the Russian Federation). As a rule, the 2-NDFL certificate is used by the income recipient:

- for registration of deductions;

- obtaining a loan;

- obtaining a visa to enter another state.

In all of these cases, you need to confirm a person’s income, and the 2-NDFL certificate is one of the most reliable sources for this.

From January 2019, it is necessary to generate a 2-NDFL certificate for employees on an updated form. It was approved by the same order of the Federal Tax Service dated October 2, 2018. The updated form has undergone technical or minor adjustments, for example, there is now no field for the reference number.

Please note that the legislation does not establish a maximum number of years preceding the requirement to issue a 2-NDFL certificate for which an employee has the right to request the document in question. A 2-NDFL certificate can be issued for the years that have passed from the date a person was hired to work until the moment of requesting the certificate, without limitation on the statute of limitations of the request.

Refusal to issue a certificate can lead to unpleasant consequences for the enterprise.

Refusal to issue 2-NDFL by the employer: consequences

If the employer does not issue the applicant with a certificate within the prescribed period, then when the latter sends a complaint to Rostrud, sanctions may be initiated against the employer under paragraph 1 of Art. 5.27 of the Code of Administrative Offenses of the Russian Federation in the form of a fine in the amount of:

- 1,000-5,000 rub. for officials, individual entrepreneurs;

- 30,000-50,000 rub. to the employer as a legal entity.

In case of repeated violation, more stringent sanctions may be applied to the employer (Clause 2 of Article 5.27 of the Code of Administrative Offenses of the Russian Federation) in the form of:

- a fine of 10,000-20,000 rubles. or disqualification for 1-3 years (for officials);

- fine 10,000-20,000 rubles. for individual entrepreneurs;

- fine 50,000-70,000 rubles. for legal entities.

True, these sanctions are applicable only if the applicant is a current employee (the provisions of Article 62 of the Labor Code of the Russian Federation, establishing the deadline for submitting 2-NDFL, do not apply to dismissed employees). But if the employer refuses to provide a certificate to a former employee, Rostrud has the right to apply sanctions to the company on the basis of Art. 5.39 of the Code of Administrative Offenses of the Russian Federation for failure to provide data upon a lawful request. Then a fine of 5,000-10,000 rubles is possible. to an official.

The 2-NDFL form issued to individuals has remained virtually unchanged. The main types of data of interest to the Federal Tax Service, which are reflected in the 2-NDFL certificate for the year, are about the income of an individual and the identity of the recipient. Let's study the features of their indication in the document.

How to correctly fill out the fields of the income certificate

The 2-NDFL certificate records only those incomes that are actually paid by the agent to the individual. If they are only accrued, there is no need to enter information about them into the certificate (unlike another important reporting document - Form 6-NDFL, which reflects both accrued and paid income).

In practice, discrepancies between actual (2-NDFL) and accrued (6-NDFL) income may indicate that the company has wage arrears. The Federal Tax Service may again notify Rostrud and law enforcement agencies about this, which will have the right to apply sanctions provided for by law to the employer.

You can find out more about such sanctions at link .

Information on income is reflected in the certificate using codes according to the list approved by order of the Federal Tax Service of Russia dated September 10, 2015 No. ММВ-7-11/387@. For example, the salary under an employment contract has code 2000. Codes for tax deductions are given similarly if they were used to reduce personal income tax during the reporting period.

For a list of income codes, see the article “List of income codes in certificate 2-NDFL (2012, 4800, etc.).”

The most valuable type of information for the Federal Tax Service in the 2-NDFL certificate is that which relates to the personality of the individual taxpayer and characterizes his income. Let's consider how this information is disclosed in the document.

We indicate information about the individual: nuances

When reflecting information about an individual taxpayer in the 2-NDFL report for the year, you need to keep in mind that:

1. If the recipient of the income is a foreigner without a Russian TIN, then the corresponding field of the certificate is not filled in. A Full Name may be filled in with letters of the Latin alphabet.

2. For the “Payer Status” field, different codes are provided for statuses that are very similar in essence. It is important to use the correct code, including:

- 1, if the taxpayer is a tax resident of the Russian Federation (regardless of citizenship);

- 2, if the payer does not have resident status (for any citizenship);

- 3, if the payer is a highly qualified worker with non-resident status;

- 4, if the person is a participant in the resettlement program with non-resident status;

- 5, if the person is a non-resident alien who has been granted asylum;

- 6, if the person is a foreigner working under a patent (resident or non-resident).

Thus, if, for example, a person participates in a resettlement program or has received asylum and become a resident, then code 1 is entered in the 2-NDFL certificate.

The taxpayer's citizenship is registered using the OKSM code (Gosstandart Decree No. 529-st dated December 14, 2001). A mark on the type of document confirming the payer’s identity is placed using the code according to Appendix 1 to the procedure introduced by Order of the Federal Tax Service of Russia dated October 2, 2018 No. ММВ-7-11/566@. The code of the subject of the Russian Federation where the payer lives is determined for the purpose of indicating it in the certificate in Appendix 2 to this procedure.

How income is reflected in the 2-NDFL certificate

When indicating information about an individual’s income, you should keep in mind that:

1. As many sections 2 and appendices to the certificate are filled in as there are types of rates that were applied when calculating personal income tax. The content of the payments does not matter: if, for example, a person received a salary and dividends at a rate of 13%, then information about both incomes is recorded in one section. Incomes are also summed up only if they are taxed at the same rate (regardless of the nature of such income).

2. When indicating income, the certificate reflects its code in accordance with Appendix 1 to Order No. ММВ-7-11/387. When indicating deductions, the code is also used - according to Appendix 2 to Order No. ММВ-7-11/387.

3. The amount of the deduction given in section 3 of the certificate should not exceed the amount of income for which the deduction was applied.

Codes for all deductions should be found in Appendix 2 to Order No. ММВ-7-11/387.

There are a number of other important, regardless of the content of the form, nuances of filling it out. Let's study them and get acquainted with an example of filling out 2-NDFL for the year.

What does an example of a 2-NDFL report look like and what else should the person filling out pay attention to?

When working with a 2-NDFL certificate, you also need to take into account that:

1. In all numeric fields in which there is no need (possibility) to reflect any total indicators, 0 is entered.

2. If the data entered into the certificate does not fit on 1 page, you must make the required number of additional copies of the certificate. In practice, this may be required if, for example, you need to provide data on different personal income tax rates.

Each copy of the certificate must indicate at the top:

- page numbers (in order);

- TIN and checkpoint.

3. If the certificate is canceling, it shall indicate:

- all information except that provided in sections 2.3 and the appendix;

- number of the certificate being canceled and the date of submission of the certificate;

- correction number 99.

4. If the certificate is corrective, it indicates:

- number of the corrected certificate and date of submission of the corrective certificate;

- the certificate number is one more than the number indicated in the original (or in the previous adjustment).

The certificate is submitted electronically if the number of recipients of income from the tax agent in the reporting period was 25 people or more (clause 2 of Article 230 of the Tax Code of the Russian Federation).

If you are interested in getting acquainted in practice with filling out the 2-NDFL certificate for the year, which is issued to an employee, you can download a sample of the finished document from the link below.

Results

Document 2-NDFL must be submitted by the tax agent to the Federal Tax Service at the end of the year and is issued to employees (including former employees) upon request. What a 2-NDFL certificate looks like for the year depends on the number of personal income tax rates applied when taxing income and the total amount of data reflected in the document. It may be necessary to submit several sheets of the report (later, perhaps, also correction or cancellation certificates).

The Ministry of Justice of Russia registered the order of the Federal Tax Service dated October 2, 2018 No. ММВ-7-11/566@, which approved the new form of the 2-NDFL certificate, the procedure for filling it out and the electronic format of this certificate. For the first time, tax agents will have to report using the new form based on the results of 2018.

Submit 2-NDFL certificates for 2018 to the tax office using the new form. The structure was changed and several fields were removed. Provide employees with information about their income on the new form “Certificate of income and tax amounts of an individual.” This form generally corresponds to the old 2-NDFL. To figure out where what information now needs to be entered, check out this table.

| Intelligence | Section where to provide information and what has changed in it |

||

|---|---|---|---|

| Old 2-NDFL of five sections | New 2-NDFL in the Federal Tax Service of three sections and an appendix | New Certificate of income and tax amounts of an individual *

of five sections |

|

| Help number | Heading at the beginning of the form | No props |

|

| Tax agent information | Section 1 | The beginning of the form (its general part) | Section 1 |

| Information about the individual - recipient of the income | Section 2 | Section 1. The section does not include the field “TIN in the country of citizenship” | Section 2. The field “TIN in the country of citizenship” was removed from section 2 |

| Information about income and deductions by month | Section 3 | Help Appendix | Section 3 |

| Standard, social and property tax deductions | Section 4 | Section 3. The section does not include the fields “Notification confirming the right to a property tax deduction”, “Notification confirming the right to a social tax deduction”. A new field “Notification type code” has appeared. It reflects code 1, 2 or 3 | Section 4. There are no fields for notification details for property and social tax deductions |

| Total income and tax amounts for the tax period | Section 5 | Section 2. The section does not include the "Notice Confirming Eligibility for Tax Reduction on Fixed Advance Payments" field. The details of this notification are reflected in section 3 | Section 5. There are no fields for the details of the notification confirming the right to reduce tax on advance payments |

* This certificate is issued to taxpayers upon their application in accordance with paragraph 3 of Article 230 of the Tax Code (Federal Tax Service No. ММВ-7-11/566 dated 10/02/2018).

How to fill out and submit 2-NDFL certificates for 2018

Since 2019, there are two forms of certificates of income and tax amounts:

- Certificate of income and tax amounts - for the tax office;

- Certificate of income in form 2-NDFL and tax amounts - for individuals upon their application.

For your attention, we offer information on how to correctly fill out 2-NDFL certificates for 2018 without errors. Various incomprehensible points in the 2-NDFL certificate are analyzed. Because due to some important errors, inspectors may ask for clarification. Download Procedure for filling out 2-NDFL

A new 2-NDFL can be generated in the updated “Legal Taxpayer”

Version 4.60 of the “” program is posted on the GNIVC website. The new version provides the ability to generate 2NDFL and 3NDFL according to the new form.

The software for generating declarations for UTII, property tax, and DAM has been improved.

The GNIVC website also contains a new version 2.136 of the Tester program.

to menu

Deadlines for submitting the 2-NDFL certificate form, where to submit it, methods of submission, who signs, presence of a stamp

Due dates

At the end of the year, the tax agent is obliged to submit a 2-NDFL certificate to the inspectorate on time.

- no later than March 1, a certificate with sign “2”. It is compiled for those individuals from whose income personal income tax cannot be withheld (for example, when giving gifts worth more than 4 thousand rubles to citizens who are not employees of the organization;);

- before April 1 with sign "1". In this case, the amount of all income received by an individual over the past year is reported; tax base from which personal income tax is calculated.

Note:

A table of reporting declarations is provided, who and when submits reports and declarations only in electronic form via the Internet in 2019

There is no responsibility for the fact that the company filled out the certificate with errors. Therefore, tax authorities can fine an organization only if the certificates are not submitted. 200 rubles each. for each missing document (clause 1). They may ask for clarification if they see inconsistencies and contradictions.

to menu

Where to submit 2-NDFL certificates

Depending on where employees or other individuals receive income. At the head office location or in a separate division.

What are the ways to submit 2-NDFL certificates for 2018?

- in electronic form via telecommunication channels;

- on paper (in person, through a representative or by mail with a list of attachments), if the number of certificates does not exceed 24 pieces.

1 . On paper: submitted to the tax office in person or sent by registered mail. This method is only suitable for those companies. In which in 2018 the number of people who received income was less than 25 Human. The certificates must be accompanied by a register of income information in two copies. One of which will remain with the Federal Tax Service.

If you submit certificates of income paid to employees on paper. Then the tax authorities, having checked these certificates, must draw up " Protocol for receiving information on the income of individuals for 2018 on paper."

This Protocol is drawn up in two copies and must be signed. Both by tax authorities and by you (if you submit 2-NDFL to the Federal Tax Service in person and not by mail). Moreover, it is not necessary to take the organization’s seal with you. The protocol will be considered valid even if only the signature of an authorized person is present. (Letter of the Federal Tax Service dated October 22, 2014 No. BS-4-11/21887@).

Having a protocol for submitting Form 2-NDFL is very important. Because it is he who confirms the fact of submitting certificates in form 2-NDFL. And also that they passed the filling control. Therefore, do not forget to pick up your copy of the Protocol from the Federal Tax Service!

2. Electronically: via the Internet (special operator, or the website of the Federal Tax Service of Russia). The number of information grouped into one file should not exceed 3000. In the first of these options, a paper register of income information must be attached to each file. One of these documents remains with the Federal Tax Service. And the other is returned to the tax agent. Having received the certificates via the Internet, the inspection will confirm the date of receipt of electronic documents with a corresponding notice the next day. Then, within 10 working days, the Federal Tax Service will send files with a register of information on income and a protocol for receiving information on income.

See the cheat sheet for those submitting 2-NDFL certificates via telecommunication channels. In the letter of the Federal Tax Service of Russia dated January 28, 2015 N BS-4-11/1208@.

to menu

Who signs 2-NDFL, stamp on the certificate

Since 2016, the rules for filling out the Certificate stipulate that it can be signed by:

- the tax agent himself (Code 1)

- his authorized representative (code 2).

In this case, you need to put the corresponding code in the help. If the Certificate is submitted to the Federal Tax Service by a representative, then the name of the document must also be reflected. Confirming the authority of this person.

There is no need to stamp the 2-NDFL certificate

The 2015 certificate required certification with a round seal. The new Certificate 2-NDFL 2019 does not provide space for printing. But if you wish, no one forbids you to put an imprint of your round seal if you have one.

Note: Letter of the Federal Tax Service dated February 17, 2016 No. BS-4-11/2577

to menu

Forms and Sample of filling out Income Certificate

FORM and EXAMPLE of certificate 2-NDFL for 2018

Note: Download form:

1. Help 2-NDFL 2018 example of filling out PDF (325 kb)

2. Help 2-NDFL 2018 example of filling out Excel (112 kb)

3. Initial data for example

4. Certificate 2-NDFL 2018 for the Federal Tax Service (blank form, Excel 100 kb)

5. Certificate 2-NDFL for an employee (blank form, Excel 100 kb)

6. Procedure for filling out 2-NDFL

FORM and EXAMPLE of certificate 2-NDFL for 2017 (after February 10, 2018)

Note: Download form:

1. Help 2-NDFL 2017 example of filling out PDF (223 kb)

2. Help 2-NDFL 2017 Excel (52 kb)

3. Help 2-NDFL 2017.xls (blank form, Excel 52 kb)

FORM and EXAMPLE of certificate 2-NDFL for 2017 (until February 10, 2018)

When drawing up a certificate of income for an individual upon their application using the form from Appendix 5 to the order of the Federal Tax Service, you can be guided by the old Procedure. Approved by order of the Federal Tax Service dated October 30, 2015 No. ММВ-7-11/485. The fact is that separate rules for drawing up this form were not approved. At the same time, the form itself, both in structure and in terms of details, almost completely corresponds to the old form 2-NDFL.

Fill out the certificate information based on the information reflected in the personal income tax registers.

Certificate 2-NDFL provides information about the tax agent.

- in section 1, indicate information about the individual in respect of whom the certificate is being filled out,

- in section 2 - information on the total amount of income, tax base and personal income tax,

- in section 3 - deductions provided to the employee,

- in the appendix - a breakdown of income and deductions by month.

If during the tax period the employee was accrued income taxed at different rates, fill out sections 1, 2 and 3, as well as the appendix for each tax rate. (clause 1.19 of the Procedure, approved by order of the Federal Tax Service dated October 2, 2018 No. ММВ-7-11/566).

It is more convenient to fill out the certificate in form 2-NDFL in the following sequence. A common part; section 1; application; section 3; section 2.

a common part

In the header of the general part, in the fields “TIN” and “KPP”, indicate the TIN and KPP of the organization. If you submit the certificates at the location of the separate unit. Then in the “Checkpoint” field, indicate the checkpoint of the separate division, TIN of the parent organization.

If the organization is the largest taxpayer. Specify the checkpoint at the place of registration of the territorial Federal Tax Service.

Organizations take the TIN and KPP from the notification of registration of the organization. Entrepreneurs indicate only the TIN. You can view it in the registration notice. Place a dash in the checkpoint field.

After the help title, provide the following information in the fields.

| Field | What to indicate |

|---|---|

| "Help number" | A unique serial number of the certificate in the reporting tax period. Assigned by the tax agent. When submitting a correction or cancellation form to replace the previously submitted one. In this field, indicate the number of the previously submitted form |

| "Reporting year" | The year for which you are issuing a certificate |

| "Sign" | 1, if the certificate is provided by a tax agent as an annual report (clause 2 of Article 230 of the Tax Code); 2, if the tax agent informs the inspectorate that it is impossible to withhold tax (clause 5 of Article 226 of the Tax Code), for example, when issuing a gift; Important! In the certificates 2-NDFL, which must be submitted by April 1. (i.e. when personal income tax was withheld from an individual), there must be a sign 1

, not 2. Otherwise, the tax office may consider that the certificates have not been submitted. Note: If you submitted certificates with sign 2, then it is safer to report on the same income by April 1. By submitting a certificate with attribute 1. 3, if the certificate is provided by the legal successor of the tax agent as annual reporting (clause 2 of Article 230 of the Tax Code); 4, if the successor of the tax agent informs the inspectorate about the impossibility of withholding tax (clause 5 of Article 226 of the Tax Code), for example, when issuing a gift |

| "Adjustment number" | 00 – when preparing the initial certificate; the value is one more than in the previous certificate - when drawing up a corrective certificate. For example, during the initial adjustment – 01, during the second adjustment – 02, etc.; 99 – when drawing up a cancellation certificate |

| “Submitted to the tax authority (code)” | The four-digit code of the tax office where the tax agent is registered. For example: 7743, where 77 is the region code, 43 is the inspection number |

| "Name of tax agent" | Indicate the abbreviated name of the organization according to the constituent documents. If there is no abbreviated name, please provide the full name. Do the same when submitting certificates to the tax authority at the place of registration of the separate division. (letter of the Federal Tax Service dated August 15, 2018 No. PA-4-11/15802) If the tax agent is an individual. In this field, indicate the last name, first name, patronymic (if any), which are indicated in the identity document. Please indicate double surnames with a hyphen (for example, Ivanov-Yuryev). Does the legal successor submit the certificate? In this case, the name of the reorganized organization is indicated in the field. Or a separate division of a reorganized organization |

| "OKTMO code" | Code of the territory in which the tax agent is registered. Determine this code using the All-Russian Classifier, approved by order of Rosstandart dated June 14, 2013 No. 159-st, or using a comparison table for OKATO and OKTMO codes. Entrepreneurs (except for UTII payers and those working under a patent), notaries, and lawyers indicate OKTMO at their place of residence. Entrepreneurs on UTII or a patent indicate OKTMO at the place of business in the appropriate special mode. If the income was paid by a separate division of the organization. Then in the certificate indicate OKTMO at the location of this unit. If during the calendar year a citizen received income in various separate divisions with different OKTMO codes. For each of them you will have to draw up a separate certificate. The legality of such a requirement was confirmed by the decision of the Supreme Arbitration Court of March 30, 2011 No. VAS-1782/11. Important: if an organization has changed its location and registered for tax purposes at a new address, please note the following. Submit separate certificates to the tax office at your new place of registration:

|

| “Form of reorganization (liquidation) (code)” and “TIN/KPP of the reorganized organization” | Filled out only by the successor, submitting certificates for the last tax period and updated certificates for the reorganized organization to the tax office at the place of registration. For the codes of the reorganization (liquidation) form, see Appendix 2 to the Procedure approved by Order of the Federal Tax Service dated October 2, 2018 No. ММВ-7-11/566. In this case, the legal successor in the certificate indicates the name of the reorganized organization and its OKTMO code |

Section 1

In section 1, provide the employee’s personal information.

In the “TIN in the Russian Federation” field, enter the employee’s TIN. Look at it in the certificate of registration of an individual. You can ask for such a document when applying for a job. Although the employee is not required to present it.

Note: The tax office is required to accept a certificate in form 2-NDFL. In which the TIN of the employee - a citizen of Russia - is not indicated. This follows from section III of the Procedure, approved by order of the Federal Tax Service dated October 2, 2018 No. MMV-7-11/566, letter of the Federal Tax Service dated August 17, 2018 No. PA-4-11/15942.

Please indicate your last name, first name and patronymic in full, without abbreviations, as in your passport. Writing in Latin letters is only allowed for foreigners. Do not fill out your middle name. Only if it is not in the passport. For foreign citizens, the last name, first name and patronymic can be indicated in letters of the Latin alphabet.

In the “Taxpayer Status” field, indicate:

– 1 – for tax residents;

– 2 – for non-residents (including for citizens of the EAEU states: the Republic of Belarus, Kazakhstan, Armenia and Kyrgyzstan);

– 3 – for non-residents – highly qualified specialists;

– 4 – for employees who are participants in the state program for the voluntary resettlement of compatriots living abroad;

– 5 – for foreign employees who have refugee status. Or received temporary asylum in Russia;

– 6 – for foreign employees who work on the basis of a patent.

In addition, for failure to submit or untimely submission of a 2-NDFL certificate at the request of the tax inspectorate, the court may impose administrative liability (Article 15.6 of the Administrative Code) in the form of a fine in the amount of:

- for citizens – from 100 to 300 rubles;

- for officials – from 300 to 500 rubles.

If the organization indicated the TIN of an individual correctly, but made a mistake in the passport data, there will be no fine. The Federal Tax Service made this conclusion in its decision dated December 22, 2016 on complaint No. SA-4-9/24731@. The decision was published on the official website of the tax service on April 10, 2017.

Decisions on complaints that the Federal Tax Service publishes on the official website are binding on tax inspectors. If you are fined for incorrect personal data of an employee in the certificate, refer to decision No. SA-4-9/24731@. Inspectors must remove the fine.

There will also be no fine if the tax agent himself discovers the error and corrects the information in a timely manner (before the inspection finds the error).

Moreover, early submission of certificates will not save you from a fine. Let’s say an organization submitted forms 2-NDFL in February. In March, the inspection discovered inaccuracies and notified the organization about it. In such a situation, even if the organization corrects all errors and submits updated certificates by April 1, it will still be fined. This procedure is provided for in paragraph 1 of Article 126.1 of the Tax Code. Similar clarifications are in the letter of the Ministry of Finance dated June 30, 2016 No. 03-04-06/38424.

to menu

The program is used to prepare taxpayers for ALL machine readable forms documents. Tax and accounting reporting. Documents used when registering taxpayers. When submitted to the tax authorities. And for preparing and uploading files any tax reporting!

Questions and answers regarding the 2-NDFL certificate. Depending on where employees or other individuals receive income. At the head office location or in a separate division. How to submit an updated 2-NDFL

To correctly fill out the 2-NDFL certificate, the “Income Codes” reference book is provided. A lot depends on the right choice of income.

Look at this table, maybe you don’t need to submit 2-NDFL certificates. Why do extra work?

-

April 17, 2015How to ask to borrow money without being refused?

April 17, 2015How to ask to borrow money without being refused? -

April 17, 2015How to open a money channel and attract good luck

April 17, 2015How to open a money channel and attract good luck