Cancellation of insurance under a collective agreement. How to return insurance after paying off a loan, in case of early repayment and during the cooling period - an algorithm of actions Terms for receiving back the insurance premium

According to current legislation An insurance contract is an agreement between the insured and the insurer, under which the insurer undertakes, when making insured event produce insurance payment to the policyholder or another person in whose favor the insurance contract is concluded, and the policyholder is obliged to pay insurance premiums on time (GK RF, Art. 929, 934, 942).

The main procedures related to the insurance contract (see Fig. 3.2):

Execution of an application for insurance;

conclusion of an insurance contract;

coordination of obligations and rights of the parties;

payment of insurance compensation;

termination of the insurance contract;

Determination of special conditions of insurance.

Insurance Application

A property insurance contract is concluded on the basis of an application from the insured, who submits to the insurer a written application in the prescribed form or verbally declares his intention to conclude an insurance contract (Article 940, clause 2 of the Civil Code of the Russian Federation).

If the insurance rules provide for the conclusion of an agreement with an inventory of property, then the inventory is attached to the application and becomes an integral part of the contract. The policyholder is obliged to give answers to all questions of the insurer concerning the determination of the degree of risk of the insured property, other circumstances known to him, related to the object of insurance.

This is necessary because the application already indicates the main economic indicators future insurance contract:

insurance value of the property offered for insurance;

· his sum insured;

the amount of insurance premiums;

insurance franchise.

According to the rules of property insurance, a period (several days) is established from the submission of an application to the signing of an insurance contract by the parties. At that time

· the policyholder makes the final decision on entering into or not entering into a contractual relationship with this insurer;

· The insurer has the right (before the conclusion of the insurance contract, as well as during its validity) to check the availability, condition and value of the property specified in the application. At the same time, the insurer checks the correctness of other information provided by the policyholder.

If insurance contracts have already been concluded for the property offered for insurance or the insured intends to conclude them with other insurers, then he is obliged to inform the insurer about this when submitting an application to him (Articles 10 and 18, clause 1b of the Civil Code of the Russian Federation).

Conclusion of an insurance contract

If both parties have not changed their decision to enter into a transaction within the period established by the rules after the submission of the application, then the procedures related to the conclusion of the insurance contract begin.

The insurer fills in an insurance contract, the content of which complies with the requirements of Chapter 48 of the Civil Code of the Russian Federation. In particular, based on the verified data of the application, the insurer enters into the contract the sum insured (including as a percentage of the insurance value) and the insurance premium.

The contract usually specifies the method of calculating the amount of the insurance premium. The basis for this is:

current tariff rates;

· declared and recorded in the contract sum insured;

Term of insurance according to the contract.

If the contract is concluded for 1 year, then the amount of the insurance premium is determined by agreement of the parties, which is based on tariff rate. The amount of the contribution in this case may be equal to the tariff, less or more than it. It depends on the ratio of supply and demand, the policy of the insurer and other reasons.

If the insurance contract is concluded for several months, then the amount of the insurance premium is calculated according to the formula:

SW n \u003d Gw p,

Where SW n - insurance premium n months; Gsv - the amount of the annual insurance premium in rubles; n – validity period of the insurance contract in months (the number of months for which the contract is concluded is expressed in the tables of insurance rules using the appropriate coefficients).

If the insurance contract is concluded for three years or more, which is currently very rare, then the insurer can provide a discount (for example, 5% or more) on the calculated amount of the insurance premium.

In addition, the property insurance contract contains sections:

· rights and obligations of the parties;

· contract time;

legal (home - for the policyholder when insuring home property) addresses of the parties.

Before signing the insurance contract, the insurer is obliged to familiarize the policyholder with the rules of property insurance and with the completed insurance contract. At the same time, the policyholder or insurer can make the necessary clarifications to the contract by mutual agreement. If this did not raise objections, then the parties sign the insurance contract and the next procedure begins - payment of the agreed amount of insurance premiums by the insured.

The procedure, form and terms of payment of insurance premiums are also established by agreement of the parties.

The policyholder or on his behalf any person may pay insurance premiums:

· in cash to the insurance agent, who is obliged to issue a receipt in the prescribed form or make a note in the insurance policy.

If the contract is for incomplete year, then the entire insurance premium is paid at a time; if - for a year or more, then the insurance premium can be paid either at a time or in installments, most often up to 4 months. In this case, the first part of the contribution is usually at least 50% of the total contribution.

If the insurer fails to pay the lump-sum contribution. or its first part within the agreed period (for example, 3 days after the signing of the insurance contract), the contract is considered not concluded. If the insured fails to pay the second part of the insurance premium within the period specified in the contract, the contract terminates upon the expiration of this period.

The policyholder is obliged to keep the documents confirming the payment of insurance premiums and present them at the request of the insurer.

After payment of insurance premiums, the procedure for the entry into force of the insurance contract begins. The contracts (and rules) of various insurers may contain the following formulas:

· when paid in cash, the insurance contract enters into force either from the moment the policyholder pays a premium (one-time or the first if paid in installments), or from 00:00 on the day following the date of payment of the premiums;

· in case of non-cash payment, the insurance contract comes into force from the moment of receipt of insurance premiums to the settlement account of the insurer, or from the day following the day of their receipt to the settlement account of the insurer;

· regardless of the form of payment, the insurance contract comes into force on the day following the date of receipt of the insurance premium (one-time or its first part if paid in installments).

As you can see, the options for determining the moment the property insurance contract comes into force are different, but the main thing in them is that without the timely payment of contributions, the contract does not enter into force and the policy will not be issued to the insured.

Within a specified period (for example, 3-5 days) after the entry into force of the insurance contract, the insurer is obliged to hand over to the policyholder an insurance policy, which must indicate:

· Title of the document;

name, legal address and bank details of the insurer;

last name, first name, patronymic or name of the policyholder and his address;

object of insurance;

the amount of the sum insured;

· Name insurance risk;

the amount of the insurance premium, the terms and procedure for its payment;

· contract time;

the procedure for changing and terminating the contract;

Other conditions as agreed by the parties, including additions to the insurance rules or exclusions from them;

· signatures of the parties.

Rights and obligations of the parties

The entry into force of an insurance contract means that the parties assume and fulfill their obligations and rights.

Obligations of the insurer:

1) familiarize the policyholder with the rules of insurance before entering into an insurance contract;

2) issue the policy to the policyholder within the terms specified in the insurance contract;

3) renegotiate the insurance contract at the request of the insured in the event that the insured takes measures that reduce the possibility of an insured event and the amount of damage to the insured property, or in the event of an increase in the actual value of the property;

4) in the event of an insured event, pay insurance compensation within the period specified in the contract (for example, 5 days) from the date of drawing up the insurance act and receiving all required documents from the competent authorities;

5) not to disclose information about the insured and his property status, except as otherwise provided by the legislation of the Russian Federation.

Rights of the insurer:

1) check the availability and condition of the insured property, as well as the correctness of the information provided by the insurant on the availability, condition and insurable value of this property;

2) refuse to pay insurance compensation in the following cases:

intentional actions of the insured, aimed at the occurrence of an insured event;

Commission by the policyholder or the person in whose favor the insurance contract is concluded, an intentional crime that is in direct causal connection with the insured event;

· communication by the insured to the insurer of deliberately false information about the object of insurance;

receipt by the insured of the appropriate compensation for damage from the person guilty of causing this damage;

untimely notification of the insurer about the insured event;

in other cases stipulated by the insurance contract.

Obligations of the insured:

1) submit to the insurer an application for insurance (2 copies) in the prescribed form with an inventory of the insured property attached as of the date of conclusion of the insurance contract;

2) pay the insurance premium in the amount, terms and procedure specified in the insurance contract;

3) immediately notify the insurer of the occurrence of an insured event and take measures to save property and preserve the remaining property until the arrival of the insurer. Immediately inform the police about the fact of deliberate actions of third parties;

4) immediately notify the insurer of all significant changes in risk relating to the insured property;

1) transfer to the insurer all available materials and documents for filing a recourse claim against the person responsible for the damage caused to the property of the insured.

The insurance contract may provide for other (other than those listed) obligations of the parties.

Rights of the insured:

1) demand the return of insurance premiums minus the costs of doing business (redemption amount) in case of termination of the contract by him unilaterally;

2) demand extradition insurance policy in the prescribed form within the period specified in the insurance contract (for example, five days after the receipt of insurance premiums to the insurer's current account);

3) require the insurer to conclude an additional insurance contract in the event of a change in the insured value of the property.

Procedure and conditions for payment of insurance compensation

Based on the legislation of the Russian Federation, the rules and insurance contracts provide for the following procedures for the procedure and conditions for paying insurance compensation:

determination of the grounds for the payment of insurance indemnities;

· determination of the grounds and methodology for calculating the amount of insurance compensation.

Basis for the decision on payment of insurance indemnity is the occurrence of an insured event corresponding to the insurance contract. Its occurrence and identification with the terms of insurance are confirmed by the following documents:

a statement of the insured about the occurrence of an insured event;

a list of lost or damaged property;

insurance certificate for loss or damage to property.

The insurance act is drawn up by the insurer or a person authorized by him within three days (excluding weekends and holidays) after receiving the application of the insured about the insured event and the list of property affected by it. If necessary, the insurer requests information related to the insured event from law enforcement agencies, the traffic police, the fire department and other competent services, bodies, institutions that have information about the circumstances of the insured event. The insurer has the right to find out the causes and circumstances of the insured event.

The basis for calculating the amount of insurance compensation are the data:

submitted by the insured

established by the insurer.

At the same time, the parties cannot dispute the insured value of the property, unless the insurer proves that he was deliberately misled by the insured.

Methodology for calculating the amount of insurance compensation and its payment is based on the following principles.

Ø First principle . It is necessary to distinguish between damage and insurance compensation.

Damage - this is the value of the lost property or the depreciated part of the damaged property, determined on the basis of the insured value (insurance valuation).

For example, the insured value of the property was estimated at 100 million rubles. Property:

a) completely died, therefore, the damage will be 100 million rubles.

rub.;

b) damaged and depreciated by 40%, therefore, the damage will amount to 40 million rubles.

At the same time, the policyholder, in accordance with the requirements of the rules, timely carried out work to save the property and put it in order in connection with the insured event. Taking into account this and other factors stipulated in the rules and contracts, in order to accurately determine the total amount of damage by fixed production assets the formula is used:

U \u003d D - I + C - O,

Where At - the total amount of damage in case of complete loss or damage to the main production assets; D – real value property under insurance assessment; AND - the amount of physical depreciation of the property on the day of conclusion of the insurance contract; WITH - expenses for saving property and putting it in order (dismantling, sorting, drying, stacking, etc.); ABOUT - the value of the remains of property suitable for further use or sale.

To determine damage on working capital the formula is used:

U \u003d D - O + C,

Where At - the total amount of damage in case of death or damage to working capital assets; D - the actual value of the property at the time of the insured event; ABOUT - the value of the remaining and usable property; WITH - the cost of salvaging property and putting it in order.

Insurance compensation determined based on damage and system insurance coverage; it is part or all of the damage payable to the policyholder in accordance with the terms of the insurance.

At proportional system insurance coverage, the insurance indemnity corresponds only to that part of the damage actually caused to the property, which was insured, for which the insured paid premiums. For example, he paid insurance premiums for 50% of the insured value of the property. Consequently, for any damage (full, partial), he will receive compensation in the amount of only 50% of the fact. Under this system, business property is insured, as well as vehicles of all forms of ownership.

With the system first risk (home contents insurance), the insured is compensated for damages in an amount not exceeding the sum insured, based on which he actually paid the insurance premiums. If the amount of damage exceeds the sum insured, the excess remains at the risk of the insured. For example, the insured value of household property is 100 million rubles, the insured amount is 50 million rubles, the damage from an insured event amounted to 70 million rubles. The insured will receive an insurance compensation of 50 million rubles, and 20 million rubles. - the second non-reimbursable risk, since he did not pay insurance premiums for it.

When determining damages under household property take into account:

· market prices of property, documented (if this is not possible, an expert assessment is made);

the physical wear and tear of the property;

the cost of loss or impairment as a result of an insured event. If any of these do not documentary evidence, then their sizes are determined on the basis of an expert assessment or in other ways according to the rules.

When determining damages under buildings, vehicles, garages the same methodology and formulas are used as for fixed production assets.

Thus, the insurance indemnity is paid by the insurer in the amount of the actual damage, but not more than the sum insured.

Ø Second principle . Payment of insurance compensation is made within the period specified in the insurance contract. For example, 3 or 5 days after the insurer establishes the causes and amount of damage that occurred as a result of an insured event.

Ø Third principle . If a criminal case has been initiated or a trial initiated on the facts related to an insured event, the decision to pay insurance compensation may be delayed until the investigation or trial is completed or the insurant's innocence is established by the investigation and court authorities.

If the insurant's innocence is confirmed by the documents of the relevant authorities, but the investigation of the criminal case or the trial continues, the insurer pays the insurer an advance, for example, in the amount of at least 50% of the amount of insurance compensation unconditionally due to him.

Ø Fourth principle . The insurer refuses to pay the insurance indemnity in the cases discussed in the "Rights of the Insurer".

Ø Fifth principle . The decision to refuse to pay insurance compensation is made by the insurer and notified to the insured in writing with justification of the reasons for the refusal.

Ø Sixth principle . If the policyholder or the beneficiary has received compensation for damage from the person who caused it to the insured property, then the insurer shall be fully or partially exempted from paying insurance compensation accordingly.

Ø Seventh principle . The policyholder or the beneficiary is obliged to return to the insurer the compensation received from him (or an appropriate part of it) if:

the person guilty of causing the damage compensated it to the policyholder in full or in part;

Within the period prescribed by law limitation period Circumstances are discovered that, by law or by the rules of property insurance (companies or citizens), completely or partially deprive the insured of the right to receive insurance compensation.

Ø Eighth principle . The insurer that has paid the insurance indemnity in connection with the insured event shall transfer the right of claim (recourse, subrogation) that the insured or other person who has received the insurance indemnity has against the person responsible for the damage caused.

Ø Ninth principle . If the policyholder, in order to increase the amount of insurance indemnity, deliberately includes in the list of lost or damaged property items that are not actually lost or damaged, then the insurer, having established this, may reduce the amount of insurance indemnity due to 50%.

Terms of termination of the insurance contract. Special conditions

According to the rules of property insurance of enterprises, citizens, reflecting the provisions of the legislation of the Russian Federation, procedures are established related to the termination of the insurance contract.

As a legal document, a property insurance contract is a specific regulator of the insurance economic relationship. The operation of insurance as an economic relationship and the insurance contract as a legal form of this relationship means the implementation by the parties of the relationship of all obligations and rights under the terms of the rules and the insurance contract. The action of the principle is characterized by the concepts: "term of insurance" and "effect of insurance".

Term of insurance means the period of time during which, according to the insurance contract or legislation, the objects are considered to be insured.

Insurance action means that in the insurance relation and the contract that issued it, the movement of their economic content begins from the moment the contract is signed by both parties and the payment of insurance premiums (premiums) by the insured, and ends

either simultaneously with the expiration of the insurance period,

or due to early termination of the insurance contract.

Termination procedures

In the movement of an insurance relationship and a contract, their end is determined with the same accuracy as the beginning, since they are associated with millions and billions of sums insured.

In various rules, there may be options for ending:

· the validity of the insurance contract is terminated at the time specified in the contract - until 00:00 on the specified day;

· the validity of the insurance contract is terminated at 24 hours of the day preceding the day from which the contract came into force, after ... years (months).

These variants differ only in phraseology. In fact, they set the same end date, for example, 00 hours on May 15 or 24 hours on May 14, when the insurance contract comes into force for a period of one year from the fifteenth of May.

Completion of insurance is associated with the termination of the insurance contract or its recognition as invalid.

Termination insurance contract according to the law has options:

1) The insurance relationship and the contract corresponding to it expire upon the expiration of the period specified in the contract and policy.

2) The insurance relationship and the contract corresponding to it are considered terminated when the insurer fulfills its obligations to the policyholder in full. For example, the contract is concluded for 1 year. The insured event occurred three months later and caused damage in the amount of the sum insured. The insurer paid the insured compensation in full in accordance with the amount of damage. This insurance contract is no longer valid.

3) The insurance relationship and the contract corresponding to it are terminated upon emergency termination of the latter for the following reasons:

non-compliance with the insurance contract by any party;

the occurrence of an insured event recorded in the insurance contract (when any of the parties considered the insurance indemnity to be unfair: to the insured - understated, to the insurer - overstated);

change of the owner of the insured property ( new owner may want another insurer or not insure property at all);

the death of the insured;

the bankruptcy of an enterprise;

liquidation of the insurer in the manner prescribed by the legislation of the Russian Federation;

· movement of the insured property from the place of permanent location specified in the policy, if such movement is not agreed with the insurer;

in other cases stipulated by the legislation of the Russian Federation.

Invalid insurance contract is recognized after acceptance judgment about this (see the Civil Code of the Russian Federation, art. 930, p. 2; 934, p. 2; 940, p. 1, etc.).

Special conditions for terminating insurance established by law and specified in the rules of insurance, while specifying the reasons for the termination and invalidity of insurance contracts.

For example:

1) The insurance contract may be terminated early at the request of the policyholder or the insurer, if this is provided for by the insurance contract or is reached by agreement of the parties:

· the parties must notify each other of their intention to terminate the contract early at least 30 days before the expected date of termination of the insurance contract, unless otherwise provided by this contract;

· the insured states his intention in the form of a written application, and the insurer - in a written communication;

· the insurance contract shall be deemed terminated from 00:00 on the day following the 30th day from the day the policyholder's application was submitted to the insurer or the policyholder's message received from the insurer;

· there may be a clause in the rules: the policyholder has the right to prematurely terminate only an insurance contract concluded for a period of at least nine months.

2) In case of early termination of the insurance contract on demand policyholder the insurer shall return to him the insurance premiums for the unexpired term of the contract, minus the expenses incurred. It is called redemption sum . If such a requirement of the insured is caused by the insurer's violation of the rules and the insurance contract, then he returns to the insured the insurance premiums paid by him in full.

3) In case of early termination of the insurance contract on demand insurer he returns to the insured the insurance premiums paid by him in full. If such a requirement of the insurer is caused by the policyholder's failure to comply with the rules and the insurance contract, then the insurer returns to him only the redemption amount - part of the contributions for the unexpired term of the contract minus the costs incurred.

4) In the event of the death of the insurant who is an individual, his rights and obligations are transferred to the person who accepted this property by way of inheritance. In other cases of replacement of the policyholder, his rights and obligations shall be transferred to the new owner with the consent of the insurer, unless otherwise provided by law or contract.

5) If during the validity period of the insurance contract the insurant, who is an individual, is recognized by the court as incapable or limited in capacity, then his rights and obligations are carried out by a guardian or custodian.

6) In case of reorganization of the insured, which is legal entity, his rights and obligations are transferred with the consent of the insurer to the appropriate successor in the manner determined by the legislation of the Russian Federation;

7) In case of loss by the insured of the insurance policy, he shall be issued a duplicate upon his written application for the period of validity of the insurance contract. After issuing a duplicate, the lost policy is considered invalid and is not subject to payment in case of insured events.

Special conditions invalidity insurance contracts specify this procedure. For example, an insurance contract is considered invalid from the moment of its conclusion:

a) in cases stipulated by the legislation of the Russian Federation;

b) and also if:

the contract was concluded after the occurrence of the insured event;

· property subject to confiscation by a court decision was insured.

Recognition of an insurance contract as invalid is substantiated by a decision of a court, arbitration or arbitral tribunal. Upon recognition of the insurance contract as invalid, the insurance premium is returned to the insured minus the costs of the insurer (redemption amount).

Disputes related to insurance are resolved by the court, arbitration or arbitration courts in accordance with their competence.

The period of validity of the insurance contract is called term of the insurance contract. To determine the term of the insurance contract, apply general provisions Civil Code of the Russian Federation: the term is determined by a calendar date or the expiration of a period of time, which is calculated in years, months, weeks, days or hours. An insurance contract can be concluded for a period of 2 hours, for a day, and so on (for example, for the duration of a sports competition).

The term of the insurance contract begins(part 1 of article 957 of the Civil Code of the Russian Federation):

1) from the moment of payment of the first insurance premium;

2) from another moment provided for in the contract (for example, from the moment of occurrence of any event).

The insurance contract is real contract, which, according to the Civil Code of the Russian Federation, begins to operate from the moment of transfer of property under it or Money. The contract may provide for a different procedure for its entry into force (Article 957 of the Civil Code of the Russian Federation), including reaching agreement on all its essential terms, and any other moment. The insurance stipulated by the insurance contract shall cover insured events that occurred after the entry into force of the insurance contract, unless the contract provides for a different period for the commencement of the insurance.

Termination of the insurance contract. Upon expiration of the period stipulated by the insurance contract, the insurance contract shall cease to be valid, and the obligations assumed by the insurer under the contract shall be considered fulfilled, even if the insured events did not occur and the insurer did not make payments. If the end of the term of the insurance contract falls on a weekend or holiday, the contract is considered to be terminated on the next business day. For example, if the term of the insurance contract ends on Saturday, April 29, and the insured event occurs on Tuesday, May 2, then the contract is considered to have expired only on Wednesday, May 3.

The insurance contract may terminate early(Article 958 of the Civil Code of the Russian Federation): the insurance contract is terminated before the date for which it was concluded, if after its entry into force the possibility of an insured event has disappeared and the existence of an insured risk has ceased due to circumstances other than an insured event. These circumstances include:

1) loss of the insured property for reasons other than the occurrence of an insured event;

2) termination in due course entrepreneurial activity a person who has insured the entrepreneurial risk or the risk of civil liability associated with this activity;

3) refusal of the policyholder (beneficiary) from the insurance contract at any time, if by the time of refusal the possibility of an insured event has not disappeared due to the above circumstances.

Thus, early termination of the insurance contract may be due to objective (not dependent on the will of the insured) or subjective reasons. objective reason is the disappearance of the need for insurance due to the termination of the possibility of an insured event due to circumstances not related to the insured event. In case of early termination of the insurance contract due to the above circumstances, the insurer is entitled to a part of the insurance premium in proportion to the time during which the insurance was valid.

In case of early refusal of the insured (beneficiary) from the insurance contract, the insurance premium paid to the insurer shall not be refunded, unless otherwise provided by the contract.

By virtue of special laws, the period of insurance is established by these laws. For example, the duration of the contract compulsory insurance owner liability vehicles(OSAGO) is 1 year, except for cases for which the same law provides for other periods of validity of such an agreement. The compulsory insurance contract is automatically extended for the next year, if the policyholder has not notified the insurer of the refusal to renew it no later than 2 months before the expiration of this contract, even if the policyholder has delayed the payment of the insurance premium for the next year (but not more than 30 days ).

An insurance premium (SP) is a monetary contribution for an insurance service due to an insurer. The transaction is fixed by the contract, and, like any agreement, it can be terminated ahead of schedule. In the article we will talk about the return of the insurance premium upon termination of the insurance contract, we will give examples of postings.

An Introduction to Insurance Premium Refunds

If the obligations of the parties under the contract are terminated due to its cancellation ahead of time, the buyer of insurance has the right to demand from the beneficiary to revise the joint venture and transfer its part back, based on the calculation of its size in its entirety and the duration of the agreement for the unfinished period, starting from the date of termination and ending with the day expiration of the policy agreement.

The legislation does not provide a reason why an insurer could withhold a larger portion of the JV than an amount proportional to the elapsed contract period.

Possible difficulties with the return of funds

In general, according to the law, it is obligatory to purchase insurance only when registering property as a pledge of a credit institution. Or the purchase of insurance is included in the main package banking product. Banks issue voluntary insurance services for mandatory ones, or they offer Better conditions loan of funds while concluding an agreement with the insurer.

There is a practice of assigning points about issuing a card, opening current accounts and servicing them by a bank in order to impose optional services on customers. You need to be careful when signing contracts, this will help to avoid some difficulties.

Problems that may arise when trying to return part of the joint venture upon termination of the contract with the insurer:

- The insurance company refers to paragraph 2, clause 3, Art. 958 of the Civil Code of the Russian Federation, assuming that the insurer no longer has any obligations to the client when unilateral refusal from his services as a policy buyer.

- Absence in loan agreement(for insurances issued upon borrowing funds from a bank) of the clause on the conclusion of an insurance agreement for the entire period of the loan agreement. This is a problem, because with this clause, the client loses obligations to the insurer immediately after the full repayment of the debt, including its early payment. Read also the article: → "".

- Absence in the insurance rules (in the section on early withdrawal from the relationship) of the conditions for calculating the remaining term of the contract. By law, this is the next day after the event that caused the early cancellation of the policy. This condition may not be indicated only when issuing an OSAGO policy, since it is assumed that the insurer terminates the contract from the date from which it became impossible for an insured event to occur.

- The loan agreement stipulates the non-return of the joint venture in case of early release of oneself from obligations.

Refunds may be denied for bureaucratic reasons:

- violation of the deadline for filing a claim,

- incorrect application,

- writing an application not in the form of an insurer,

- lack of documents confirming the legality of the early termination of the agreement.

Ways to get your insurance premium back

Early withdrawal from relations with the insurance company may occur for objective reasons, when the contract is no longer able to be executed due to the absence of the object of insurance, and for subjective reasons, if the policyholder has expressed a desire to stop working with the insurer.

Full and partial refund of insurance premiums:

- A full refund is possible if the insured has paid off the loan with the bank within 1-2 months.

- A partial refund is likely if six months have passed since the loan was issued. If the amount of the insurance premium exceeds one hundred thousand rubles, it makes sense to ask the insurer for an extract with a distinction according to the targeted distribution of funds

In case of refusal to pay money, you can redirect a written refusal to Rospotrebnadzor or go to court with a statement of claim.

If the court decides in favor of the plaintiff, it makes sense to shift the litigation to the insurance company and demand compensation for moral damages for the illegal use of the misappropriated joint venture for commercial purposes. The court usually takes the side of the consumer of the service, based on the unreasonableness of paying the full cost of the service to the insurer with only partial performance.

If the insurance company recognizes a debt to the purchaser of the policy equal to the cost of the JV after the termination of obligations under the agreement before the agreed time, the insurer will return the JV not included in the costs in full. This is explained by the fact that a certain share of the tariff (namely 23%) is his expenses under the OSAGO agreement. The Ministry of Finance allows firms to account for this part of the funds as an expense when paying corporate income taxes.

Deadline for claiming insurance premium back

- Usually, it takes a month and a half to study applications for the return of a joint venture from the bank in which the loan and the insurance service agreement were drawn up, moreover, you need to apply with an application within a month, otherwise only part of the funds paid on account of insurance can be returned.

- When leaving an application for the return of a joint venture with the insurance company itself, you need to be prepared for a 30-day wait for a decision.

Accounting entries for the return of insurance premiums

Basic provisions:

- The money spent on transport insurance (OSAGO, CASCO) is included in the list of expenses for ordinary activities. They are added to the cost of products sold and affect account 76-1 “Settlements for property and personal insurance". Read also the article: → "".

- On the day when the company sends money as a joint venture to the insurance company, the accountant is obliged to record the advance payment (this is Debit 76-1 Credit 51 - paid by the joint venture).

- The cost of insurance funds is not subject to VAT.

- The insurance policy expense item begins to be recognized by accountants from the moment the joint venture payments begin, if it turned out that the agreement does not mention a specific date from which the agreement is recognized as valid.

- If the contract is calculated for a period of more than 30 days, the accountant makes a monthly posting: Debit 20 (23/26/44 ..) Credit 76-1 - the cost of the joint venture for the current month is charged to expenses.

- If the agreement is designed for a period of less than a month, the joint venture must be added by the accountant to the costs of the month in which the agreement was recognized as valid. Debit and Credit see clause 5-a.

- If the organization began using the services of the insurance company not from the 1st day of the month, the amount is subject to write-off in proportion to the number of days remaining until the end of the month.

- The returned funds of the unspent joint venture should be reflected in the posting: Debit 51 Credit 76-1 - part of the insurance received. premiums, taking into account the actual duration of the contract.

A practical example of BU and NU when returning an insurance premium

Organization N on the simplified tax system “Income minus expenses” acquired the ownership of a passenger vehicle and spent money on OSAGO and CASCO. Less than a year later, it was resold. Under NU, the price of OSAGO was added to expenses, in accounting - to expenses for the duration of the contract with the insurer (1 year) on account 97, was debited to account 20. CASCO was not included in NU, but actions with OSAGO were repeated in BU.

So, at the beginning of the next year, there was a balance on Debit 97 of the account, the costs of issuing the policy were not written off. Bought soon after new car, and the insurer carried over the unspent insurance amount to new policies.

Tax accounting for this case. On the date when the tax accounting of the organization was carried out, the accountant had to reflect 2 transactions:

- The balance of funds that were transferred by the insurer back to the company's account as an excess payment of the JV under the insurance contract terminated ahead of schedule with it, are included in the number of incomes subject to accounting when paying a single tax;

- The same amount of funds is taken into account in the list of expenses for insurance services under the second contract.

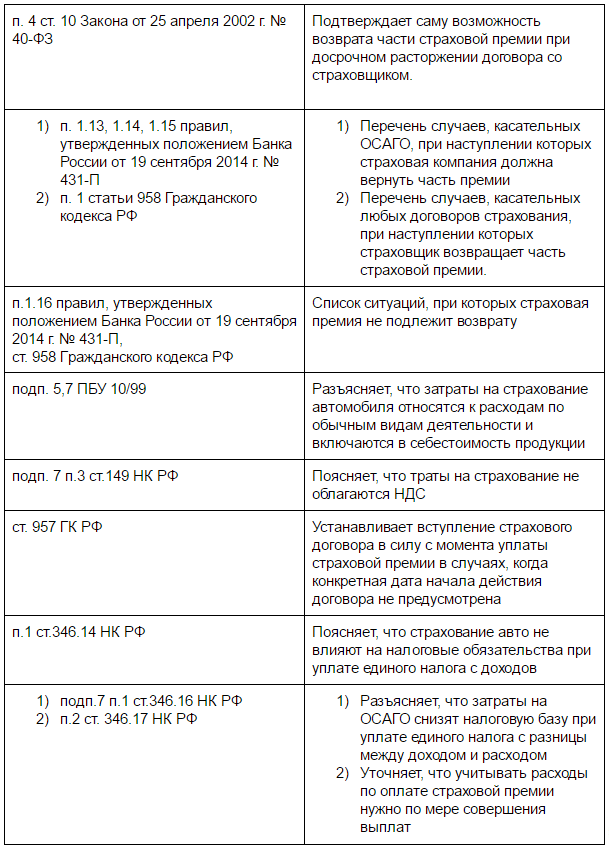

Normative acts regarding the return of the insurance premium:

An example of calculating the returned insurance premium

An organization on the simplified tax system “Income minus expenses” uses a vehicle for the needs of the company and transfers money under an OSAGO agreement paid for the year (from 02/01/15 to 01/31/16). Annual fear. the premium is 4 thousand rubles. and is paid by the company at a time on 1.02.15. Calculating the EH for the first quarter of 2015, the accountant adds these 4 thousand rubles to the expenses. And on March 2, 2015, the car was resold, and the contractual relationship was terminated.

Then, on March 10, 2015, the insurer will return to account N SP in the amount of 3682 rubles, focusing on the actual term of the agreement. When accruing EH for the first quarter of 2015, the company's accountant will add the returned money (3682 rubles) to the income.

Typical errors when trying to return

Mistake #1. When writing an application for the return of the joint venture, it is indicated that the insured wants to terminate the contract with the insurance company ahead of schedule.

Such a case will fall under clause 3, paragraph 2, Art. 958 of the Civil Code of the Russian Federation (unilateral termination of the agreement, refusal of insurance), which provides for the refusal to partially pay the joint venture. If we take insurance when issuing a loan by a bank as an example, then the joint venture will not return to the borrower if he refuses insurance without having time to repay the loan.

Mistake #2. Recognition as an expense of the amount of the joint venture that remained in the list of deferred expenses after the sale by the company vehicle for which the insurance was issued.

This amount of money should be reflected in accounts receivable the insurer, after which measures must be taken to collect the debt. If the money is not returned due to a statute of limitations or debt forgiveness, the funds are listed as unrealized expenses as uncollectible debts.

FAQ

Question number 1. The company paying the tax under the “simplification” “Income minus expenses” took into account the returned part of the JV when paying taxes in the period when it was transferred to the account. What to do if a promissory note was issued on account of its payment?

Such income must be taken into account at the time of payment of the bill or its transfer by endorsement to another person.

Question number 2. What is the number to indicate the payment of the insurance premium after the early termination of cooperation with the insurer, if an agreement was concluded with him on the fulfillment of counter obligations by offset?

The date of income is the day of certification of the act of offsetting.

Question number 3. Can an insurance company return part of the JV through an electronic wallet?

Yes. In this case, the settlement system operator will reduce the balance electronic money from the sender and increase their amount from the recipient at the same time.

Case No. 2-295/2016

SOLUTION

IN THE NAME OF THE RUSSIAN FEDERATION

Anzhero-Sudzhensky City Court Kemerovo region composed of:

presiding Gulnova N.V.,

under the secretary Voroshilova I.G.,

having examined in open court in the city of Anzhero-Sudzhensk

civil case on the suit Kremneva K.The. to PJSC "Sberbank of Russia", LLC IC "Sberbank life insurance" on the recognition of the insurance contract as null and void, the return of the insurance premium, interest for the use of other people's money, compensation for moral damage, a fine,

SET UP:

Kremnev K.V. filed a lawsuit against Sberbank of Russia PJSC to declare the insurance contract null and void, return the insurance premium, interest on borrowed money, compensation for non-pecuniary damage, and a fine.

He motivates his claims by the fact that on May 14, 2015, loan agreement No. 353966 was concluded, according to which Sberbank of Russia OJSC provides him with a loan in the amount of<...>rubles, for a period of 36 months, at 19.5% per annum. Prior to the conclusion of the loan agreement, they submitted an application for a loan in the amount of<...>rubles. According to paragraph 10 of the loan agreement, the borrower's obligation to provide security for the performance of obligations under the agreement and the requirement for such security are not applicable to the agreement. However, when concluding a loan agreement, a representative of the bank orally offered him participation in the collective insurance program, the services of which are provided by Insurance Company Sberbank Life Insurance LLC (hereinafter referred to as the insurance company). To participate in the collective insurance program, the claimant must sign an application for insurance on voluntary life, health and in connection with the involuntary loss of work of the borrower NPRO No. No. (hereinafter referred to as the application for insurance). Participation in the group insurance program, according to the representative of the bank, is prerequisite to receive a loan, and in case of refusal to participate in the collective insurance program, the bank will not provide the loan service, despite the fact that the application for insurance regulates that refusal to participate in the collective insurance program will not entail a refusal to provide banking services.

According to the application for insurance, the bank provides services for connecting the borrower to the collective bargaining agreement voluntary insurance concluded between the insured OJSC Sberbank of Russia and the insurer OOO Sberbank Life Insurance Insurance Company, by extending to the plaintiff the Conditions for joining the borrower's collective life and health insurance program as part of the issuance of a consumer loan by the bank.

The bank increased the loan amount by<...>rubles, which is the insurance premium under the insurance contract, and is calculated according to the formula: Sum insured * tariff for connecting to the Insurance Program * (number of months / 12), i.e.<...>

He was granted a loan by the bank by transferring to account No. opened in accordance with clause 9 of the loan agreement in the amount<...>rubles. from his account No. without acceptance, the bank debited the insurance premium in the amount<...>rubles.

In his opinion, the insurance contract and the loan agreement are interconnected: in the application for insurance, the amount of the insurance premium is calculated from the sum insured equal to the amount of the loan. These circumstances confirm the direct relationship between the loan agreement and the borrower's insurance, i.e. the conclusion of a loan agreement without fail causes accession to the insurance agreement.

The requirements of the loan agreement and the application for insurance are contrary to the law due to the following: he is not given the opportunity to get acquainted with the life insurance service with other insurance companies; the insurance program concluded between OJSC Sberbank of Russia and the insurer LLC Insurance Company Sberbank Life Insurance, created specifically for OJSC Sberbank of Russia, indirectly confirms the impossibility of concluding life insurance with another insurance company; he was not acquainted with the insurance contract, which should indicate the sum insured and remuneration; the insurance policy was not issued; he is not familiar with the license of Insurance Company Sberbank Life Insurance LLC. These circumstances violate the law "On the Protection of Consumer Rights", namely Art. Art. 10,12,16.

An indication in the application for insurance for voluntary life and health insurance of borrowers for clients of Sberbank of Russia Open Joint Stock Company that: “I am aware that participation in the program of voluntary life, health insurance and in connection with the involuntary loss of the borrower’s job and my refusal to participate in The insurance program will not result in a refusal to provide banking services. This clause cannot be valid and the application itself cannot be considered voluntary for the following reasons: an application for insurance for voluntary life and health insurance of borrowers for clients of Sberbank of Russia OJSC is made within the framework of a loan agreement and, in essence, is an application to LLC Insurance Company " Sberbank life insurance, whose responsibilities include only insuring customers, and not issuing a loan, the application cannot be considered a fundamental document for issuing a loan. The application for insurance on voluntary life and health insurance of borrowers for clients of Sberbank of Russia says: “I confirm that I have been provided with all the necessary and essential information about the insurer and the insurance service, including with the conclusion and execution of the insurance contract” , it does not indicate what kind of information is provided to the borrower. He was not acquainted with the conditions of insurance, rules of insurance, the insurance contract, the procedure and deadlines for submitting applications for termination of the insurance contract. The Bank did not provide him with information in an accessible and visual form on the amount of the insurance premium to be transferred to the insurer, as well as on the amount of the bank's commission for connecting to the insurance program. Joining the insurance program is a stand-alone service and is not a method of collecting so-called hidden interest.

25.01.2016 he sent to the bank an application for the return of the insurance premium on the application for insurance NPRO No. dated 05/14/2015. 28.01.2016 they received a refusal to return the illegally received insurance premium.

He believes that the insurance contract concluded in respect of him between JSC "Sberbank of Russia" and the insurer LLC Insurance Company "Sberbank Life Insurance" on the application for insurance NPRO No. dated 14.05. 2015, is void by virtue of Art. , Art. Law of the Russian Federation "On Protection of Consumer Rights" that the amount of illegally debited funds is subject to return. He also believes that the actions of the defendant caused him moral harm, which he assesses as<...>rub.

He asks the court to recognize the insurance contract concluded in relation to him between OJSC Sberbank of Russia and the insurer LLC Insurance Company Sberbank Life Insurance on the application for NPRO insurance No. dated, void, to oblige OJSC Sberbank of Russia to return to him losses in the amount of<...>rubles, transferring them to his account No., to recover compensation for non-pecuniary damage in the amount of<...>rubles, interest for the use of other people's funds in the amount of<...>rubles for the period from to, a fine of 50% of the amount awarded in his favor.

Determination of the Anzhero-Sudzhensky City Court dated 02.02.2016. when accepting the statement of claim for proceedings, Limited Liability Company Insurance Company Sberbank Life Insurance was involved as a co-defendant in the case.

At the hearing the plaintiff Kremnev K.The. claim and the arguments set out in the statement of claim, supported. He explained to the court that he had been lending at Sberbank for more than 15 years, had always fulfilled the obligations of the loan agreement, had a positive credit history. Works in the system<...>paid a one-time allowance in the amount of seven salaries payroll, in connection with which, upon the occurrence of these events, the amount of payment to him is several times higher than the amount of payment taken by him from the bank under the loan agreement, that is, he has a real opportunity to repay the loan debt, as well as interest on borrowed funds. In this connection, the bank did not have a real need for additional risk insurance when issuing a loan to it. When imposing additional insurance by the bank, the bank pursued only the goal of obtaining additional profit in the form of an insurance premium, putting it in conditions where it could not exercise its right to voluntarily life and health insurance. Also, the bank did not give him the right to choose an insurance company in order to purchase insurance services on more favorable terms for him. Having received a loan in the amount<...>rubles, he will have to pay the bank a significant amount, taking into account the insurance received. The service provided for connecting the borrower to the Insurance Program is an independent financial service Bank, other than insurance services. The service provided by the bank for connecting it to the insurance program is single and indivisible both in its essence in general and for the consumer in particular. He affixed his signature to every item in the statement, as it standard document, he wanted to get a loan, he needed money. The procedure for joining the voluntary insurance program, including the right to terminate the insurance contract within 14 days, was not explained to him, and no additional documents were given to him. He was unable to get a loan without insurance.

At the hearing, the representative of the defendant - Batanina E.D., acting on the basis of a power of attorney, did not recognize the claim, submitted a written response. Court explained that 14.05.2015 g. between the plaintiff Kremnevym K.The. and PJSC Sberbank of Russia signed a loan agreement No. 353966, under which Kremnev K.V. funds have been provided<...>rub. When concluding a loan agreement, Kremnev K.V. it was proposed to insure their life and health against accidents for the period of the contract. For three years, the insurance premium amounted to<...>. PJSC "Sberbank of Russia" did not impose Kremnev K.V. insurance service in Ltd. Insurance company «Sberbank life insurance», since the insurance is voluntary, is carried out on the basis of an application for insurance, which the plaintiff Kremnev K.The. signed voluntarily. There was no coercion on the part of the defendant's employees. Kremnev K.V. was familiarized with the conditions of participation in the program of collective voluntary insurance of borrowers of individuals of Sberbank of Russia PJSC, was subsequently connected to this program, also one copy of the conditions for participation in the program of collective voluntary insurance of borrowers of individuals of PJSC Sberbank of Russia, a memo to the insured person were issued Kremnev K.V. on your hands. In addition, participation in the Insurance Program may be terminated if the client refuses insurance on the basis of an application submitted within 14 days from the date of joining the Insurance Program. At the same time, the client is refunded funds in the amount of 100% of the amount of the connection fee, which the plaintiff did not use within these terms. Kremnev K.V. could refuse insurance altogether, it is voluntary and receive a loan under the same conditions, or choose any other insurance company at your discretion. Sberbank of Russia PJSC offers its customers the products of IC Sberbank Life Insurance LLC. The client has the right to either agree to insurance, or refuse, and also apply to another insurance company at his discretion, there are no obstacles to this.

The representative of the defendant LLC Insurance Company Sberbank Life Insurance did not appear in court, was duly notified of the place and time of the hearing, and did not report the reasons for the failure to appear to the court.

After listening to the parties, the witness, having studied the materials of the case, the court comes to the following conclusions.

DECIDED:

In satisfaction of the claims of Kremnev KV against PJSC Sberbank of Russia, LLC IC Sberbank Life Insurance on the recognition of the insurance contract concluded in respect of it by JSC Sberbank of Russia and LLC IC Sberbank Life Insurance as void on the application of NPRO No. dated 14.05. 2015, the obligation of PJSC "Sberbank of Russia" to return the insurance premium in the amount of<...>rubles, collection of interest for the use of other people's funds in the amount of<...>rubles for the period from to, compensation for non-pecuniary damage in the amount of

Arbitrage practice on the application of Art. 454, 168, 170, 177, 179 of the Civil Code of the Russian Federation

For loans, for loan agreements, banks, bank agreement

Judicial practice on the application of the norms of Art. 819, 820, 821, 822, 823 of the Civil Code of the Russian Federation

Under insurance contracts

Judicial practice on the application of the norms of Art. 934, 935, 937 of the Civil Code of the Russian Federation

Content

When applying for a loan to many potential borrowers, the bank offers to conclude an insurance contract. If it is impossible to settle the client's debt, the insurance company must close his debt to the bank. Often the opposite situation occurs, conscientious payers have questions: in case of early repayment of the debt, is it possible to return the insurance on the loan to the insured borrower, can the bank or insurer return the money upon application and to what extent?

What is credit insurance

Before returning the insurance premium on a loan, you need to understand the essence of such insurance. In order to reduce its own risks of non-repayment, the bank offers to conclude an insurance contract to the client who has applied for the issuance of credit resources. When agreeing to such an offer, it is necessary to distinguish between the voluntariness and obligatory nature of the insurance service that accompanies a consumer loan, because the borrower pays considerable amounts for each policy.

Compulsory insurance

Legally, the insurance condition accompanying the receipt of a loan is not mandatory for the borrower and remains his voluntary choice. However, there are exceptions. When providing property as collateral for a loan, the pledge is necessarily insured under the following types of loan agreements:

- Car loans. When applying for a car loan, a credit institution has the right to oblige the borrower to issue CASCO for the purchased vehicle.

- Mortgage credit lending. When issuing a loan secured by real estate and registration mortgage loan The collateral is covered by insurance.

Voluntary insurance

Other types of insurance that accompany the conclusion of consumer lending are voluntary for the borrower. You can collect insurance on a loan under agreements of the following type (according to them, as a rule, credit institutions impose insurance):

- life and health of a citizen (death, disability, incapacity);

- job loss;

- title insurance for mortgages;

- financial risks;

- other property of the borrower in addition to the car and real estate.

Legal Legislation

Since June 1, 2016, the conditions for voluntary insurance have been changed in favor of the borrower, and the individual has the opportunity to return the money by terminating the imposed insurance after the loan is repaid. This is legally documented:

- Instruction of the Central Bank of the Russian Federation No. 3854-U “On the minimum (standard) requirements for the conditions and procedure for the implementation of certain types of voluntary insurance”;

- Civil Code RF (Article 343);

- Federal Law No. 353 “On consumer credit (loan)” (part 10, article 7);

- Federal Law No. 102 “On Mortgage (Pledge of Real Estate)” (Article 31);

- Federal Law No. 4015-1 "On the organization of insurance business in the Russian Federation" (Article 3, paragraph 4).

Is it possible to get credit insurance back?

According to the new rules in the field of credit law, the bank should not insist on registration additional services. However, there are two different situations: cancellation of the insurance contract prior to receiving a loan, and return of insurance after the loan is repaid. In both cases, the citizen has the right to refuse the service, and even after the conclusion of a contractual relationship with the insurance company. However, financial institutions are in no hurry to pay out insurance on credit obligations.

In what cases is the refund of the sum insured not possible?

Despite important changes for insured borrowers, there are a number of situations where the question of how to return insurance after paying off a loan remains problematic and is often resolved in court:

- Terms of the conclusion of the contract. The rules effective from 06/01/2016 apply to new contracts. It is not possible to receive compensation for the cost of insurance under existing insurance contracts.

- Collective insurance. The norms of the Law are valid if a citizen enters into an agreement directly with the insurance company. If credit institution the service is concluded within the framework of a collective agreement, it does not fall under the possible return of insurance on a loan in five days.

- Choice of loan option. If the bank offers two lending models for the client to choose from - without insurance at a higher interest rate or with insurance, but at lower interest rates, and the borrower chose the second option, then his decision regarding insurance is voluntary.

- Conditions of the insurance contract. If the insurance conditions do not provide for the return of unused loan insurance upon termination of the insurance contract ahead of time, it is possible to repay the loan ahead of schedule, but the rest of the unused remuneration will remain with the insurers.

What documents must be provided to the insurer

If you had to issue consumer credit with the payment of the insurance policy imposed on you by the bank, in order to return the money, contact the insurance company with a package of the following documents:

- loan agreement (original and copy);

- passport;

- an application for refusal of voluntary insurance indicating the method of receiving payment or an application for terminating the contract ahead of schedule and returning the insurance in the remaining part;

- bank certificate of early closing of the debt (if the loan was repaid ahead of schedule).

How to return the loan insurance in the first 5 days after signing the loan agreement

The indication of the regulator of the insurance and credit market, the Bank of Russia, determined the time period, the cooling period, for applying for an insurance premium - 5 business days. Important: during these five days, the insurance may come into force, then a smaller amount is due for the return of the insurance on the loan than was paid. If you meet the deadline, the whole process goes like this:

- The citizen, within five working days after signing the contract, applies to the insurer with a statement of refusal from the concluded voluntary insurance contract with the designation of details for receiving funds.

- From the insurer, it is imperative to obtain a visa on acceptance for consideration on your copy of the application or send it by registered mail with an inventory and return notification.

- After ten days, the borrower must return the funds.

Features of the procedure for collective agreements

The new rules do not apply to collective insurance. The peculiarity of this type is that the insured is not individual and the bank and the borrower join the contract. In this case, read the contract and insurance rules in order to familiarize yourself with other conditions for refusing paid insurance. Credit institutions and insurance companies are developing their own conditions, providing for early dissolution under collective insurance, when the loan is repaid: there may not be an opportunity to return the money ahead of schedule.

Return of insurance in case of early repayment of the loan

It makes sense to deal with the return procedure if the insurance premiums were paid in advance. Insurance protection of the collateral or life of a citizen is needed in case of an unpaid loan, and if the borrower repays it ahead of schedule, then the return of insurance after the early payment of the loan is possible in the remainder of the insurance service. In this situation, it is initially necessary to contact the bank, which has the right to send the citizen to the insurance company to resolve the issue. An application for a refund of funds is made simultaneously with an application for early repayment of a loan or immediately after its closing.

How to get a refund for insurance on a loan after a “cooling off period”

If the prescribed five days have passed, contact the bank first. The return of insurance on a loan is possible in an extended period at certain credit institutions: Sberbank, VTB24, Home Credit Bank, but not everyone is so loyal. For example, Alfa-Bank, Renaissance Credit do not offer such a service to customers. According to the claim sent to the bank, most likely, a refusal will be received on the basis of the voluntary signing of the insurance application by the borrower. Then there is only a judicial way to resolve the issue, and it is advisable to seek help from credit lawyers.

Application for return of insurance to the bank

As a rule, the bank and the insurer have their own ready-made samples of filling out documents. When applying to the bank, it is important that the form contains the following information:

- Title of the document;

- Full name, passport information, address of the client;

- date of signing;

- place of registration;

- signature;

- information about the loan agreement (number, validity period, amount) and repayment of obligations (date of actual payment);

- details to be paid.

Going to court

This option is suitable for a small part of people. The current judicial experience in challenging imposed insurance services is negative, but the practice of resolving the issue in Moscow and across Russia in identical cases is different. Claims of this kind relate to the field of consumer protection, which means that the citizen chooses the place of filing the statement of claim (the place of registration of the mortgage, the location of the beneficiary). That is, you can stop at geographic region, where similar court cases ended positively in favor of the plaintiff.

Video

Did you find an error in the text? Select it, press Ctrl + Enter and we'll fix it!-

April 17, 2015Lifebuoy for builders

April 17, 2015Lifebuoy for builders -

April 17, 2015What is investment and how is it beneficial?

April 17, 2015What is investment and how is it beneficial? -

April 17, 2015Consumer loan rate

April 17, 2015Consumer loan rate