Help for a tax deduction for a child form. Application for the standard tax deduction for children. Standard deduction per child - application

The standard tax relief for personal income tax in the form of a deduction for a child is provided at the place of work. For its application, the employee is required to provide his management with an application with a corresponding request. A sample application, relevant for 2018, can be downloaded in the article below.

There are many nuances and features in the design of a children's deduction. All questions are sorted out, the information is relevant for 2017.

An application from an individual with a request to apply the standard personal income tax deduction to his income, which is due if there are children of a suitable age in the family, is the main document that the worker must present to his employer in order to use the benefit.

Its compilation does not have strict regulations; a standard form has not been developed. The employee needs to take a blank sheet of paper and write the text in a request-notification form with his own hand.

Documents must be added to the application that can confirm what is stated in the paper. Depending on the situation, the set of attached documentation may vary.

In the simplest case, it is enough to provide copies of birth certificates. If the child is disabled, a medical certificate is attached. Single parent claims double deduction.

If the minor is adopted, taken under guardianship or guardianship, has exceeded the threshold of 18 years and is studying full-time, as well as in some other situations, additional documents are required. A copy is made of all and attached to the application.

It is enough to write an application once and submit it to the management. The form does not need to be updated annually. A new spelling is possible if something has changed in the amount of the standard personal income tax benefit for this employee, for example, he has another child, or the husband (wife) has waived his right to the deduction, giving the second spouse the opportunity to receive double the amount.

How to write correctly in 2018

The form of the text is free, but it is necessary to include information sufficient for the employer on the size of the standard tax benefit, the number and age of children, and the attached documents.

In particular, the text should read:

- request to provide a standard deduction;

- Full name of each child, his age, details of the birth certificate (children of all ages are listed, regardless of whether they are deductible or not, the employer needs this information to correctly calculate the amount of personal income tax benefits);

- size - indicated in relation to those children who have such a right;

- a list of documents that are transmitted along with the application;

- reference to the paragraph of the Tax Code of the Russian Federation, where the possibility of a standard deduction is prescribed (clause 4, clause 1, article 218 of the Tax Code of the Russian Federation).

You need to address the application to your management, which is noted in the upper right part of the paper sheet.

You need to certify the text with your personal signature indicating the date of its affixing.

If the application for the deduction for children is submitted late, then for the months of the current year the employer will return income tax, and for the months of last year, you need to contact the Federal Tax Service for a refund of personal income tax.

When changing location labor activity for a new employer, you must also write applications for a child income tax deduction. Plus, you need to provide a certificate of 2-personal income tax from a previous employer. This certificate will allow the new employer to correctly calculate the amount of total income from the beginning of the year, since there is a restriction on it.

The deduction for children is provided only until the annual income reaches the mark of 350,000 rubles. If the total salary since the beginning of January of the current year has reached this bar, then the employer does not take into account this indicator until the end of the year. The countdown starts over from the new year.

Actual sizes in 2018:

- 1st, 2nd - 1400 for each;

- 3rd, 4th and further - 3000 for each;

- if a child with a disability of 1 or 2 gr. - a deduction of 12000 (for a natural parent), 6000 (for a foster parent) is added.

Download Sample

Sample application for a standard tax deduction for personal income tax for children -

Upon receipt of remuneration, an employee-resident of the Russian Federation pays personal income tax in the amount of 13%. Income tax can be reduced by submitting to the employer an application from an individual for a tax deduction:

- standard tax deduction ();

- property();

- social();

- professional().

Making standard invoices

Employees with disabilities, participants in hostilities, people affected by radiation, as well as parents, adoptive parents and guardians of children can reduce the tax. We give the size in the table:

To receive a tax credit, you must submit a written application for a tax deduction. It is also necessary to provide the employer with documents confirming the right to tax reduction, for example, a birth certificate, certificates of disability, etc.

An up-to-date sample application for a tax deduction in 2020 for children

Making a property deduction

To reduce the base for personal income tax by the cost of purchased housing and mortgage interest, it is necessary to provide the employer with a special notice from the Federal Tax Service.

To obtain this document from the tax office, you will have to apply for a notification on property deduction 2020. You also need to provide documents confirming the right there, according to the list:

- contract of sale;

- mortgage agreement;

- act of acceptance and transfer of the apartment;

- payment documents.

The company will reduce the personal income tax base by an amount not exceeding that specified in the notification.

An up-to-date sample application for a property deduction from an employer:

You can get benefits not only through the employer. It is permissible to apply to the Federal Tax Service by submitting an application for a property tax deduction.

Professional benefits

On this basis, personal income tax can be reduced when performing work or providing services under a civil law contract or receiving royalties for the creation of literary, musical, artistic, and other works, as well as the invention of models and industrial designs. The amount is determined either in the amount of the costs incurred, or according to the standards established in clause 3.

If, for some reason, the employer calculated personal income tax from the full amount of income, then at the end of the year you can submit a 3-personal income tax declaration to the FTS inspection and return the overpaid tax.

Social deductions for treatment and education

To reduce tax on this basis, it is also necessary to submit a form - a sample application for a tax deduction refund 2020, and supporting documentation. Then get a notification from the IFTS. Recall that, in accordance with personal income tax deductions, you can get on:

- education;

- treatment;

- payment of additional contributions to a funded pension;

- expenses for voluntary insurance: retirement and life.

A deduction for charitable expenses or independent evaluation employee qualifications can only be obtained by filing a 3-NDFL declaration at the end of the reporting year.

Completed tax return form:

How to return the tax through the Federal Tax Service?

Taxpayers have the right to apply directly to the territorial office tax service. This possibility is enshrined in the Tax Code of the Russian Federation. That is, citizens will have to choose how to receive a fiscal deduction.

In order to qualify for a personal income tax refund through an inspection, you will have to collect a package of documents that confirm the rights to benefits. Note that the registration of benefits through the Federal Tax Service can only be started in the next year, after the year in which the grounds for applying the fiscal deduction arose. For example, if you have the right to a benefit in 2020, then you can apply to the IFTS only in 2020.

In this case, you need to draw up a tax return 3-NDFL.

The fiscal report contains personal details payer, income information, and the amount of personal income tax to be returned. In addition to the declaration and copies of supporting documentation, you will have to fill out a special form. For example, an application for a tax refund for a property deduction.

Note that such a written appeal can be issued in any form:

The state in order to support the ongoing population policy fixed in the tax legislation a kind of benefit: a tax deduction for personal income tax for children. Why is personal income tax or income tax taken? Because this is exactly the obligation that almost all citizens fulfill before the state. Russian Federation with the exception of pensioners - no income tax is withheld from the pension.

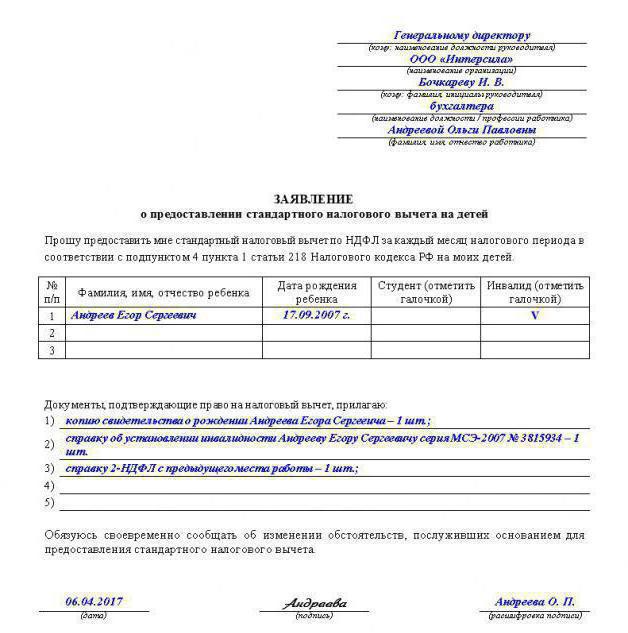

Application for a tax deduction for children: sample

Like all other benefits, the provision of tax deductions is carried out exclusively through an application from the applicant. It must be written to the accounting department of the enterprise where the parent is officially employed. The tax deduction is equally granted to both the father and the mother in a single amount established by the tax legislation. If the child is raised by one parent, then the deduction based on the submitted application will be provided in double the amount.

A standard sample application for a tax deduction for children can be obtained from the accounting department. Otherwise, the application can be made in free form, indicating the following details and personal data:

- the name of the enterprise (tax agent) where the parent works;

- surname, name, patronymic of the parent;

- surnames, names, patronymics of children for whom a tax deduction should be provided;

- children's age;

- for students over 18 years of age - the name of the educational institution in which the child is studying on a full-time basis;

- date and signature of the applicant.

Attention! Applications for granting a deduction are written annually! There is no deduction for a child over 24, even if they continue to study full-time!

Supporting documents

The application must be accompanied by a package of supporting documents for the tax deduction for children. These will be:

- photocopies on paper of the birth certificates of all children;

- for students over 18 years of age - the original certificate from the educational institution attended by the child;

- a copy of the death certificate of the spouse (for single parents raising children). Single mothers do not need supporting documents on marital status - information about it is provided to the employer ( tax agent) upon employment;

- if any of the children has a disability - the original certificate from doctors about its presence.

How much will the benefit be?

The deduction sizes are different:

- for the first and second child - monthly 1400 rubles per child for each parent;

- for the third and all subsequent children - monthly 3,000 rubles per child for each parent;

- if the child has a disability - monthly at 12,000 rubles until he turns 18 years old. If he studies full-time, then up to 24 years;

- if a child with a disability is adopted, then monthly at 6,000 rubles.

I would like to note that these tax benefits are provided not only to biological parents, but also to any legal representative: guardian, foster parent, adoptive parent.

In order to determine the amount of the deduction for the second or third child, do not forget that all born and adopted children are taken into account, regardless of age. If the oldest of the three children is already 25 years old, then who, for example, is 16 years old, will be provided in the amount of 3,000 rubles. Therefore, it is important for the applicant to list all children (regardless of age) in the child tax credit application. A sample of such information may not contain.

Finally

So, summarizing all of the above, we note the following:

- The tax legislation provides certain benefits to families with children.

- Sample applications for a tax deduction for children can be obtained from the accounting department or found independently on the Internet.

- All children must be listed on the application to qualify for the exemption.

One of the standard tax deductions is the deduction for the taxpayer, which is provided to certain individuals, for example, "Chernobyl victims", disabled since childhood, parents and spouses of dead military personnel. Full list individuals who may qualify for a standard deduction is specified in paragraphs. 1, 2, 4 article 218 of the Tax Code of the Russian Federation.

Taxpayers entitled to more than one standard tax deduction are granted the maximum of the applicable deductions. The deduction for children is provided regardless of the provision of other standard tax deductions.

Types of standard tax deductions

Standard tax deductions:

deduction for the taxpayer

This type of standard tax deduction is provided to 2 categories of individuals listed in paragraph 1 of Art. 218 of the Tax Code of the Russian Federation.

deduction per child(ren)

The deduction for a child (children) is provided up to the month in which the taxpayer's income taxed at the rate 13%

and calculated on an accrual basis since the beginning of the year, exceeded 350,000 rubles. The deduction is canceled from the month when the employee's income exceeded this amount.

- for the first and second child - 1400 rubles;

- for the third and each subsequent child - 3000 rubles;

- for each disabled child under 18, or a full-time student, graduate student, intern, intern, student under the age of 24, if he is a disabled person of group I or II - 12,000 rubles to parents and adoptive parents (6,000 rubles - to guardians and trustees).

If the spouses, in addition to a common child, have a child from early marriages, the common child is considered the third.

Procedure for obtaining a tax deduction for a child (children)

Provided to taxpayers who support a child (children).

Write an application for a standard child tax credit (children) to the employer.

Prepare copies of documents confirming the right to receive a deduction for a child (children):

- certificate of birth or adoption (adoption) of a child;

- certificate of disability of the child (if the child is disabled);

- a certificate from an educational institution stating that the child is a full-time student (if the child is a student);

- document on registration of marriage between parents (passport or marriage registration certificate).

If the employee is a single parent (single foster parent), it is necessary to supplement the set of documents with a copy of the document certifying that the parent is the only one.

If the employee is a guardian or guardian, it is necessary to supplement the set of documents with a copy of the document on guardianship or guardianship of the child.

- decision of the body of guardianship and guardianship or an extract from the decision (decree) of the said body on the establishment of guardianship (guardianship) over the child;

- an agreement on the implementation of guardianship or guardianship;

- an agreement on the implementation of guardianship over a minor citizen;

- foster family contract.

Contact your employer with an application for a standard tax deduction for a child (children) and copies of documents confirming the right to such a deduction.

To correctly determine the amount of the deduction, it is necessary to line up the order of children according to their dates of birth. The first born child is the oldest child, whether or not a deduction is granted.

If the taxpayer works simultaneously for several employers, the deduction at his choice can be granted only with one employer.

An example of calculating the amount of tax deduction for children

Matveeva E.V. four children aged 16, 15, 8 and 5 years old.

At the same time, her monthly income (wage) is 40,000 rubles.

Matveeva E.V. filed a written application addressed to the employer for a standard tax deduction for all children: for the maintenance of the first and second child - 1,400 rubles each, the third and fourth - 3,000 rubles a month.

Thus, the total amount of the tax deduction amounted to 8,800 rubles per month.

Every month from January to August, the employer will count on his employee Matveeva E.V. Personal income tax from the amount of 31,200 rubles received from the difference in taxable income at a rate of 13% in the amount of 40,000 rubles and the amount of a tax deduction in the amount of 8,800 rubles:

Personal income tax \u003d (40,000 rubles - 8,800 rubles) x 13% \u003d 4,056 rubles.

Thus it is on the hands of Matveeva E.The. will receive 35,944 rubles.

If Matveeva E.V. did not apply for a deduction and did not receive it, then the employer would calculate personal income tax as follows:

personal income tax = 40,000 rubles. x 13% \u003d 5,200 rubles, income for deduction of personal income tax amounted to 34,800 rubles.

In some cases, for example, for a single parent, the amount of the deduction can be doubled. At the same time, the fact that the parents are divorced and the alimony is not paid does not mean that the child does not have a second parent and is not a basis for receiving a double tax deduction.

The procedure for obtaining a tax deduction if during the year the standard deductions were not provided by the employer or were provided in a smaller amount

If during the year the standard deductions were not provided by the employer or were provided in a smaller amount, the taxpayer has the right to receive them when submitting a personal income tax return to tax authority place of residence at the end of the year.

In this case, the taxpayer must:

Obtain a certificate from the accounting department at the place of work on the amounts of accrued and withheld taxes for the corresponding year in the form 2-NDFL.

Prepare copies of documents confirming the right to receive a deduction for a child (children).

Provide the tax authority at the place of residence with a completed tax return with an application for a standard tax deduction and copies of documents confirming the right to receive a standard tax deduction.

* If the submitted tax return has calculated the amount of tax to be refunded from the budget, submit an application for a tax refund to the tax authority (together with tax return, or at the end of cameral tax audit).

The amount of overpaid tax is subject to refund at the request of the taxpayer within one month from the date of receipt by the tax authority of such an application, but not earlier than the end of the in-house tax audit (clause 6, article 78 of the Tax Code of the Russian Federation).

When submitting copies of documents confirming the right to deduction to the tax authority, you must have their originals with you for verification by the tax inspector.

09.07.19 11 698 0

standard deduction This is the amount that is not subject to personal income tax. In other words, the state allows not to pay personal income tax on the income received or returns the tax already withheld.

You can receive a standard deduction for yourself or for children. Full list those who can receive a deduction for themselves, is indicated in tax code. For example, disabled people from childhood, Chernobyl survivors, participants in the Second World War, parents and spouses of dead servicemen have the right to a deduction.

Sizes of standard deductions

The size of the standard tax deduction varies depending on the category of the taxpayer.

"Chernobyl victims" and citizens affected by the accident at the Mayak plant, who participated in the testing of nuclear weapons and the elimination of radiation accidents, military personnel, war invalids and some other categories of people are entitled to a standard deduction of 3 thousand rubles for each month of the calendar year.

Heroes of the USSR and the Russian Federation, military personnel and members of their families, invalids of childhood and war, and some other categories of persons are entitled to a standard deduction of 500 rubles for each month of the calendar year.

Parents, including adoptive parents, guardians and trustees are entitled to a tax deduction for each child up to 18 or 24 years old, for disabled child 1 or 2 groups.

The amount of the deduction varies depending on the number of children and the composition of the family:

- for the first and second child to the parent, including the adoptive parent, guardian, trustee - 1400 R;

- for the third and each subsequent child - 3000 R;

- on the disabled child under 18 or disabled child up to 24 years of group 1 or 2, if he studies full-time, to the guardian, trustee and foster parent - 6000 R;

- for each disabled child under 18 or disabled child up to 24 years of group 1 or 2, if he studies full-time, to a parent or adoptive parent - 12,000 R.

The standard double deduction is due to the only parent or one of the parents, if the second one refused the deduction and received a certificate of this at work. If the parents are divorced, this does not entitle one of them to receive the standard double deduction by default, without the second declaring to waive the deduction.

A parent receives a tax deduction for a child until the month in which his total income exceeds 350 thousand rubles. With a salary of 40 thousand rubles a month, the parent will receive a deduction from January to August inclusive. With a salary of 70 thousand rubles a month - until May inclusive.

The deduction will be given until the child turns 18. If the child is studying full-time, then the deduction will be extended for the entire period of study, but maximum until the child turns 24 years old.

If you are entitled to a deduction on several grounds, then maximum deduction from suitable ones. But at the same time, a deduction for children is always provided, regardless of whether you receive another deduction or not.

On the third disabled child you can get a deduction in the amount of 15 thousand rubles: 3 thousand rubles for the third child and 12 thousand rubles for disability.

Documents for obtaining a standard deduction

To deduct for yourself

- A copy of the document confirming the right to payment: certificate of disability of group 1 or 2, certificate of a war veteran or other document, depending on the benefit.

- An application for a deduction must be filled out on the spot.

To deduct for children you will need the following documents:

- A copy of the birth or adoption certificate of the child or children.

- A copy of the marriage registration certificate or passport page with a marriage mark.

- Certificate of full-time education, if the child is a student.

- Certificate of disability if the child is disabled.

- Help 2-NDFL from the previous place of work, if you got a job not from the beginning of the year.

The single parent additionally submits documents confirming the right to a double standard deduction:

- A copy of the death certificate of the second parent, an extract from the court decision on recognizing the parent as dead or missing.

- A copy of the passport page on marital status without a marriage mark.

- Certificate in form No. 2, if the father is entered in the birth certificate of the child according to the mother. If there is a dash in the child's certificate in the column "father", such a certificate is not needed.

The adoptive parent or guardian collects the following documents:

- Decree of the body of guardianship and guardianship.

- An extract from the decision of the specified body on the establishment of guardianship (guardianship) over the child.

- A copy of the agreement on guardianship or guardianship.

- A copy of the foster family contract.

If you forgot to write an application for a deduction from your employer or wrote, but not for all children, you can return part of the tax paid. Write an application for a tax refund from the employer.

If you are not working, you can return the tax deduction. Contact your nearest tax office with the following documents:

- Copies of documents confirming the right to a standard deduction.

- Certificate in the form 2-NDFL from the place of work for the previous year.

- Declaration in the form 3-NDFL, filled in on the spot.

- Application to be filled out on the spot.

-

April 17, 2015What affects the credit rating of organizations

April 17, 2015What affects the credit rating of organizations -

April 17, 2015The fiscal function of taxes is expressed in the fact that

April 17, 2015The fiscal function of taxes is expressed in the fact that

")