When it is possible to combine the STS with other taxation systems (basic, envd, eskhn, etc.). Taxation of farms: comparison of regimes of the main usn eshn Types of activities that fall under eshn

The unified agricultural tax (ESAT) is a tax paid by producers of agricultural goods when they voluntarily switch to this special tax regime (clause 1, clause 2, article 346.1 of the Tax Code of the Russian Federation).

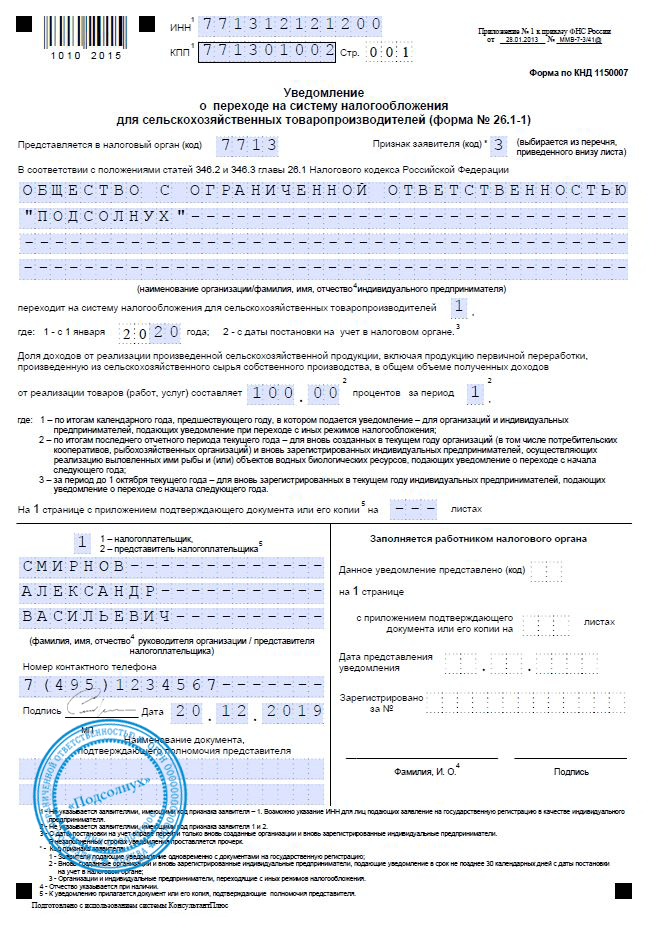

In order to switch to a special regime in the form of paying the Unified Agricultural Tax, organizations and entrepreneurs need to notify the tax office at the place of their registration (clause 1, article 346.3 of the Tax Code of the Russian Federation).

If we talk about the ESHN (what it is in simple words), then this is a special regime for producers of agricultural goods, which allows you to pay tax at a lower rate, simplify reporting and document flow.

ESHN: taxation

Organizations applying a special tax regime for agricultural producers are exempt from paying corporate income tax, corporate property tax, except for the situations specified in paragraph 3 of Art. 346.1 of the Tax Code of the Russian Federation. Entrepreneurs who have switched to the use of the Unified Agricultural Tax are exempt from paying personal property tax, personal income tax in relation to income received from entrepreneurial activity, with the exception of the situations specified in paragraph 3 of Art. 346.1 of the Tax Code of the Russian Federation.

Until January 1, 2019, agricultural producers applying the Unified Agricultural Tax were exempted from paying VAT, with the exception of the situations specified in paragraph 3 of Art. 346.1. But starting from January 1, 2019, a change in the tax legislation of the Russian Federation obliges organizations and individual entrepreneurs that have switched to the Unified Agricultural Tax to calculate and pay VAT in the general manner in accordance with Ch. 21 of the Tax Code of the Russian Federation (clause 12, article 9 of the Federal Law of November 27, 2017 N 335-FZ, Letter of the Federal Tax Service of May 18, 2018 No. SD-4-3 / [email protected] ).

Also, payers of the ESHN of the Tax Code of the Russian Federation are obliged to pay transport tax and other taxes (for example, water tax) if they have the appropriate objects of taxation.

Single agricultural tax in 2019

The UAT is calculated based on the results of half a year, the amount of tax is determined as the difference between income and expenses multiplied by the tax rate (clause 1, article 346.6, clause 2, article 346.7, clause 1, clause 2, article 346.9 of the Tax Code of the Russian Federation).

The tax rate of the Unified Agricultural Tax is set at 6% (clause 1, article 346.8 of the Tax Code of the Russian Federation). At the same time, the laws of the subjects may establish differentiated rates ranging from 0 to 6% for all or certain categories of taxpayers, depending on: the types of agricultural products produced, the amount of income, the place of business and / or the average number of employees.

The payment of the ESHN, as well as the advance payment on it, is made by organizations (IEs) at the place of their registration (clause 4, article 346.9 of the Tax Code of the Russian Federation). In this case, the advance payment for the ESHN is paid no later than the 25th day of the month following the half year (clause 2 of article 346.7, clause 2 of article 346.9 of the Tax Code of the Russian Federation). The tax itself is paid no later than March 31 of the next year (clause 5 of article 346.9 of the Tax Code of the Russian Federation, clause 2 of article 346.10 of the Tax Code of the Russian Federation).

Upon termination of activities as producers of agricultural goods, the UAT must be paid no later than the 25th day of the month following the month in which such activities are terminated, according to the notification sent to the Federal Tax Service (Clause 2, Article 346.10 of the Tax Code of the Russian Federation).

Deadline for payment of ESHN in 2019:

Tax declaration for the unified agricultural tax

The tax declaration for the UAT is submitted by organizations (IP) in this special regime at the end of the year to the tax office at the place of their registration no later than March 31 of the next year (clause 1, article 346.7, clause 1, clause 2, article 346.10 of the Tax Code of the Russian Federation ).

Upon termination of activities as producers of agricultural goods, it is necessary to submit a tax return for the UAT no later than the 25th day of the month following the month in which such activities are terminated, according to a notification sent to the Federal Tax Service (IFTS).

Foundation and legal basis

The system of taxation in the form of ESHN - the single agricultural tax - is one of the five special tax regimes. It is intended for use in agriculture, as the name suggests.

Like all other special regimes, the ESHN replaces the payment of income tax and VAT, and the ESHN also replaces the payment of corporate property tax.

The unified agricultural tax was introduced by chapter 26.1 of the Tax Code of the Russian Federation. Reporting forms, as usual, are established by the financial department. Also, the legal framework for the UAT can include explanations from the Ministry of Finance and the Federal Tax Service of the Russian Federation - these explanations are not of a regulatory nature, but help to understand various aspects of the application of the tax.

The procedure for switching to ESHN

The transition to a single agricultural tax is a voluntary matter. It is necessary to decide on the desire to apply the EAT by December 31 of the year preceding the year from which the EAT will be applied. It is during this period - until December 31 - that you need to submit a notification to the tax authority at your location (place of residence). It contains data on the share of income from the sale of agricultural products produced by the taxpayer.

A newly created organization or a newly registered individual entrepreneur has the right to notify of the transition to the payment of unified agricultural tax no later than 30 calendar days from the date of registration with the tax authority indicated in his certificate.

Pay attention!

Special conditions for notification of the transition to the Unified Agricultural Tax are established by Article 346.3 of the Tax Code of the Russian Federation for organizations that are included in the unified state register of legal entities on the basis of Article 19 of the Federal Law of November 30, 1994 N 52-FZ.

Organizations and entrepreneurs that have not submitted a notification of the transition to UAT payment within the established time limits are not recognized as UAT payers and, accordingly, will not be able to apply this taxation regime in the new year.

Taxpayers who switched to paying the unified agricultural tax are not entitled to switch to other taxation regimes until the end of the tax period.

If at the end of the tax period the taxpayer ceases to comply with the above mandatory conditions, then he is considered to have lost the right to apply the unified agricultural tax from the beginning of the year in which this violation was committed or revealed.

If the taxpayer has lost the right to apply the UAT, he is obliged to inform the tax authority about the transition to a different taxation regime within 15 days after the expiration of the reporting (tax) period.

Taxpayers have the right to switch from UAT to another taxation regime from the beginning of a new calendar year. To do this, you must again notify the tax authority at the location of the organization (or the place of residence of the individual entrepreneur) no later than January 15.

Taxpayers who have switched to a different taxation regime are entitled to switch back to paying the Unified Agricultural Tax no earlier than one year after the loss of the right to apply it.

Taxpayers

UAT taxpayers- These are organizations and individual entrepreneurs that are agricultural producers and have switched to paying a single agricultural tax in the manner prescribed by the Tax Code of the Russian Federation.

Agricultural producers can be:

- Organizations and individual entrepreneurs:

- producing agricultural products;

- carrying out its primary and subsequent (industrial) processing (including on leased fixed assets);

- selling these products.

All of the above conditions must be met at the same time. If a company does not produce agricultural products, but only buys it, processes it and sells it, then they will not be able to become a UAT payer.

A prerequisite for switching to the UAT is that based on the results of work for the calendar year preceding the year in which the application for the transition to payment of the UAT is submitted, the share of income from the sale of agricultural products produced must be at least 70% of the taxpayer's total income.

- Agricultural consumer cooperatives - if, based on the results of their work for the previous calendar year, the share of their income from the sale of agricultural products of their own production by members of these cooperatives, as well as from work (services) for members of these cooperatives, is at least 70% of the total income.

- Town- and village-forming Russian fisheries organizations, the number of employees in which, taking into account family members living with them, is at least half of the population of the corresponding settlement. For them, the following conditions are mandatory (for the transition to the ESHN):

- in the total income from the sale of goods (works, services) for the previous year, the share of their income from the sale of their catches and (or) fish and other products produced on their own from them is at least 70%;

- they carry out fishing on the vessels of the fishing fleet owned by them, or use them on the basis of charter agreements (bareboat charter and time charter).

- Fishery organizations and individual entrepreneurs.

Mandatory conditions for the transition to the ESHN:

- the average number of employees, for each of the two calendar years preceding the filing of the notification, does not exceed 300 people;

- in the total income from the sale of goods (works, services), the share of income from the sale of their catches of aquatic biological resources and (or) fish and other products from aquatic biological resources produced on their own from them for the previous year is at least 70%.

A complete list of agricultural producers who are entitled to switch to the payment of the Unified Agricultural Tax is indicated in Article 346.2 of the Tax Code of the Russian Federation.

Not entitled to switch to the payment of the unified agricultural tax:

- organizations and individual entrepreneurs engaged in the production of excisable goods;

- organizations engaged in organizing and conducting gambling;

- state, budgetary and autonomous institutions.

Agricultural products for the purpose of taxation of the UAT include:

- crop production of agriculture and forestry;

- livestock products, incl. obtained as a result of growing and growing fish, as well as other aquatic biological resources.

The closed list of agricultural products was approved by Decree of the Government of the Russian Federation of July 25, 2006 N 458.

Tax exemption

Organizations that have switched to paying the Unified Agricultural Tax are exempted from the obligation to pay:

- corporate income tax;

- corporate property tax;

Individual entrepreneurs who have switched to paying the Unified Agricultural Tax are exempted from the obligation to pay:

- personal income tax (in relation to income received from entrepreneurial activity);

- tax on property of individuals (in relation to property used for entrepreneurial activities);

- value added tax (with the exception of VAT payable when goods are imported into the territory of the Russian Federation and other territories under its jurisdiction).

Other taxes and fees are paid in accordance with the legislation of the Russian Federation on taxes and fees.

Pay attention!

Organizations and individual entrepreneurs who are payers of the unified agricultural tax are not released from the duties of tax agents.

Object of taxation and tax base

The object of taxation under the Unified Agricultural Tax is income reduced by expenses. The procedure for determining income and expenses is established by Article 346.5 of the Tax Code of the Russian Federation.

The tax base is the monetary value of income reduced by the amount of expenses.

The date of receipt of income is the day of receipt of funds to bank accounts and (cash desk), receipt of other property (works, services), property rights, as well as repayment of debt in another way (cash method).

Costs are recognized as costs after they are actually paid.

Incomes and expenses in foreign currency are recalculated into rubles at the exchange rate of the Central Bank of the Russian Federation, established respectively on the date of receipt of income (the date of expenses). Incomes received in kind are taken into account on the basis of the contract price, taking into account market prices determined by the rules of Art. 105.3 NK.

The tax base can be reduced for the tax period by the amount of the loss received as a result of previous tax periods. Taxpayers have the right to carry forward the loss to future tax periods within 10 years following the tax period in which this loss was incurred.

Organizations are required to keep records of their performance indicators necessary for calculating the tax base and the amount of unified agricultural tax, based on accounting data.

Individual entrepreneurs may not keep accounting records, but they are obliged to keep records of income and expenses for the purposes of calculating the tax base for the UAT in the book of income and expenses of individual entrepreneurs using the UAT. The form and procedure for filling out this book are approved by Order of the Ministry of Finance of Russia dated December 11, 2006 N 169n.

Pay attention!

Taxable period

The tax period is a calendar year.

The reporting period is half a year.

tax rates

The tax rate for the UAT is set by the Tax Code at 6% and is generally unchanged.

However, since 2015, for Crimea and Sevastopol, the possibility of lowering the UAT rate has been introduced. For the period 2015-2016 these regional authorities could reduce the rate to 0%. For the period 2017-2021 reduction is possible only up to 4%.

In 2016, both in Sevastopol and in the Republic of Crimea, a tax rate was set at the Unified Agricultural Tax in the amount of 0.5%.

In 2017, by the Laws of the Republic of Crimea and the city of Sevastopol, the UAT rate was increased to a minimum of 4%.

Pay attention!

According to paragraph 2 of Art. 346.8 of the Tax Code of the Russian Federation, the UAT rate established by the laws of Crimea and Sevastopol for 2017 will not increase until 2021, that is, during this entire period it will be equal to 4%.

The procedure for calculating and paying ESHN. Reporting

When applying the ESHN, the tax is calculated as a percentage of the tax base corresponding to the tax rate. The taxpayer must calculate the tax himself according to the rules established by the Tax Code of the Russian Federation.

Based on the results of the reporting period, it is necessary to calculate the amount of the advance payment, based on the tax rate and the actual income received, reduced by the amount of expenses calculated on an accrual basis from the beginning of the tax period to the end of the half year. The advance payment must be paid no later than 25 calendar days from the end of the reporting period.

After the expiration of the tax period, taxpayers submit tax returns and pay unified agricultural tax to the tax authorities:

- organizations - at their location;

- individual entrepreneurs - at their place of residence.

You must submit your tax return and pay tax for the previous year no later than March 31 of the year.

The tax return form was approved by order of the Federal Tax Service of Russia dated July 28, 2014 N ММВ-7-3 / [email protected] It can be submitted both in paper and electronic form.

Upon termination of activity as an agricultural producer, an organization or an individual entrepreneur must pay tax and submit a declaration for the UAT no later than the 25th day of the month following the one in which, according to the notification, the activity was terminated.

Pay attention!

Taxpayers whose average number of employees for the previous calendar year exceeds 100 people, as well as newly created organizations whose number of employees exceeds the specified limit, submit tax returns and calculations only in electronic form. The same rule applies to the largest taxpayers.

You can see more about electronic reporting.

A complete list of federal electronic document management operators operating in a particular region can be found on the official website of the Office of the Federal Tax Service of Russia for the constituent entity of the Russian Federation.

ESHN: what's new in 2017?

From January 1, 2017, taxpayers applying the Unified Agricultural Tax can take into account the costs of conducting an independent assessment of the qualifications of employees. The corresponding changes were made by the Federal Law of July 3, 2016 N 251-FZ in paragraphs. 26 p. 2 art. 346.5 of the Tax Code of the Russian Federation.

In 2017, by the Laws of the Republic of Crimea and the city of Sevastopol, the UAT rate was increased to the minimum possible 4% and, in accordance with paragraph 2 of Art. 346.8 of the Tax Code of the Russian Federation, the UAT rate will no longer increase until 2021, that is, during this entire period it will be equal to 4%.

Pay attention!

When paying arrears for all taxes, from October 1, 2017, the rules for calculating penalties will change. In case of a long delay, large amounts of penalties will have to be paid - this applies to arrears that arose after October 1, 2017. Changes have been made to the rules for calculating penalties, which are established for organizations in paragraph 4 of Art. 75 of the Tax Code of the Russian Federation.

If, starting from the specified date, the payment is overdue by more than 30 days, the interest will be calculated as follows:

- based on 1/300 of the refinancing rate of the Central Bank of the Russian Federation, effective from the 1st to the 30th calendar days (inclusive) of such a delay;

- based on 1/150 of the refinancing rate of the Central Bank of the Russian Federation, relevant for the period starting from the 31st calendar day of delay.

In case of delay of 30 calendar days or less, the legal entity will pay penalties based on 1/300 of the refinancing rate of the Central Bank of the Russian Federation.

The changes are provided for by the Federal Law of May 1, 2016 N 130-FZ.

If arrears are paid before October 1, 2017, the number of days of delay does not matter, the rate in any case will be 1/300 of the Central Bank refinancing rate. Recall that since 2016 the refinancing rate is equal to the key rate.

Tell me, please, what is the difference between the simplified taxation system and the UAT in 2020?

Firstly, the UAT can be used by organizations that either produce agricultural products, or process and sell them, as well as other organizations or individual entrepreneurs that provide support services to producers of such agricultural products regarding livestock or crop production. In a word, in order to use the UAT, you must be engaged in activities directly related to agricultural products.

For the simplified tax system, the list of activities in which you can use this tax system is much wider. Moreover, in order to switch to the simplified regime, your income must be no more than 112.5 million rubles for the nine months of the previous year, and the income itself during the period of using the simplified regime must not exceed 150 million rubles a year.

Also, for the tax period, the average number of your employees should not be more than one hundred people. The branches specified in the Charter of the LLC must also be absent.

If we talk about the tax rate, then according to the USN "Income" it is six percent, but in certain regions it can be reduced to one percent, and in Crimea and Sevastopol - to zero. The rate for ESHN is equal to six percent, and can also be reduced in the Crimea and Sevastopol, but only up to four percent.

Can I reduce my taxes by the amount of any costs if I use the simplified tax system when I register an individual entrepreneur? The same question applies to the ESHN.

If you are an individual entrepreneur and use the simplified income tax system, then in this case the tax can be reduced by the amount of insurance premiums, benefits paid for temporary disability of employees (with the exception of occupational diseases) and voluntary insurance. Also, the tax can be reduced by the amount of insurance premiums paid by the individual entrepreneur for himself. If you have employees in the state, then the tax can be reduced on insurance premiums for employees and for yourself, but not more than 50 percent. If you work without hired employees, then the amount of tax can be reduced by the amount of contributions paid for yourself and without any restrictions.

When using the single agricultural tax, the tax base is reduced only at the expense of expenses.

You can prepare documents for registering an individual entrepreneur with Internet access in 10-15 minutes with the free My Business service. It is enough to provide basic information about yourself. At the exit, you will receive an application filled out in accordance with all the rules and a receipt for payment of the state duty.

Is there any marginal income for me that I can receive while on simplified tax or agricultural tax?

Yes, there really is such a limit for the simplified taxation system. It is 150 million rubles a year. There are no such restrictions for the ESHN, but there is a rule that the share of income from the sale of agricultural products cannot be less than 70 percent of the total sales income.

With what frequency and how should I pay tax on the ESHN or on the simplified tax system?

If you use the USN 6% system, then advance payments for this tax must be transferred to the tax authority every quarter, and the total amount - at the end of the year. As for the ESHN, you must transfer advance payments every six months, and the final amount is exactly the same at the end of the year. VAT is paid no later than the 25th day of each month following the quarter.

The simplified taxation system is used by taxpayers along with other taxation regimes. This is stated in paragraph 1 of Art. 346.11 of the Tax Code of the Russian Federation.

However, in practice, an organization can only combine the simplified tax system with UTII. And individual entrepreneurs can combine "simplification" with both UTII and the patent taxation system.

So, it is impossible to work simultaneously on the simplified tax system and on the general taxation system, since each of these regimes applies to all types of activities that the taxpayer conducts.

The "simplification" is also incompatible with the ESHN due to a direct indication of this in paragraphs. 13 p. 3 art. 346.12 of the Tax Code of the Russian Federation.

In addition, the USN is not entitled to apply organizations that are engaged in the gambling business and pay tax on the gambling business.

It is also impossible to combine "simplification" with the taxation system when fulfilling production sharing agreements. After all, the participants in such an agreement are not transferred to the simplified tax system (clause 11, clause 3, article 346.12 of the Tax Code of the Russian Federation).

Thus, at the same time, an organization can only apply the simplified tax system and UTII. "Vmenenka" is applied voluntarily in relation to the types of activities for which the taxpayer switched to paying UTII and was registered with the inspection, provided that this special regime was introduced in the relevant territory (Article 346.28 of the Tax Code of the Russian Federation). Therefore, if in relation to the types of activities listed in paragraph 2 of Art. 346.26 of the Tax Code of the Russian Federation, UTII is applied, then for other types of activities the organization has the right to apply the simplified tax system.

USN and UTII can be applied by an organization and for one type of activity specified in paragraph 2 of Art. 346.26 of the Tax Code of the Russian Federation, but at the same time, separate subdivisions (objects) through which such activities are carried out should not be located:

On the territory of one municipal district;

- on the territory of the federal cities of Moscow and St. Petersburg;

- in the territory of several districts of one city district.

Thus, the combination of UTII and STS for one type of activity is unacceptable for objects that are located:

- on the territory of one municipality;

- in the territory of one city of federal significance.

Let's give an example, organization "X" is engaged in wholesale trade and applies the simplified tax system. It also sells goods at retail in the territory where a taxation regime in the form of UTII has been introduced for retail trade. In such a situation, for retail, organization "X" can apply UTII, and for wholesale - USN.

It should be noted that when combining the USN and UTII, it is necessary to keep separate records (clause 7 of article 346.26 of the Tax Code of the Russian Federation).

Individual entrepreneurs can combine the simplified tax system not only with UTII in the manner described above, but also with the patent taxation system. The patent system of taxation is applied to the types of activities for which an individual entrepreneur has received a patent. For other activities, you have the right to apply the simplified tax system.

As a general rule, organizations that apply the simplified tax system do not pay income tax (paragraph 1, clause 2, article 346.11 of the Tax Code of the Russian Federation).

However, this exemption does not apply to certain types of income. Therefore, with some of them you must pay tax yourself and submit reports to the tax office. For other taxable income, this will be done for you by a tax agent - the person from whom you received such income.

So, when working on the simplified tax system, income tax is paid on the following income (paragraph 1, clause 2, article 346.11 of the Tax Code of the Russian Federation):

1) from dividends.

Moreover, if a Russian organization paid you dividends, then it acts as a tax agent, i.e. must withhold income tax from these incomes and transfer it to the budget (clause 2, article 275 of the Tax Code of the Russian Federation). Thus, in this case, you do not need to pay the tax yourself.

If you received dividends from a foreign organization, you must calculate and pay income tax on them in the general manner.

2) from interest on securities specified in paragraph 4 of Art. 284 of the Tax Code of the Russian Federation, namely:

- on government securities of the member states of the Union State (the Russian Federation, the Republic of Belarus);

- government securities of subjects of the Russian Federation;

- municipal securities;

- mortgage-backed bonds.

3) from the income of the founders of trust management of mortgage coverage received on the basis of mortgage participation certificates.

You must calculate and pay the tax yourself.

In addition, when receiving income from which you must pay income tax under the simplified tax system on your own, you need to file a declaration for this tax with the tax authority.

Diana Demina

dealt with ESHN

Anton Dybov

tax expert

ESHN - single agricultural tax.

This is a tax regime for producers who work in crop production, animal husbandry, forestry and agriculture. This regime exempts individual entrepreneurs and companies from paying several taxes:

- income tax. An exception is the tax on dividends and certain types of debt obligations for LLCs.

- personal income tax for IP.

- Property tax if it is used in agricultural business.

We tell you who and under what conditions can work for the ESHN. The article will help to understand the general points, but for the nuances we recommend contacting an accountant.

Who can work for ESHN

To work on the ESHN, organizations and individual entrepreneurs must meet the following requirements:

- Engage in the production, processing and sale of agricultural products. The key word is production. If you buy raspberries from a farmer and make jam out of it, you won’t be able to switch to ESHN.

- The share of income from agricultural activities must be at least 70% of all income. These are all incomes that came from agricultural OKVED codes. For example, code group 01 refers to crop production, animal husbandry, and 03 to fisheries.

And this is a list of organizations and individual entrepreneurs who are prohibited by law from working for the ESHN:

- Producers of excisable goods, such as alcohol or perfumes.

- Representatives of the gambling business.

- State and budgetary institutions.

In simple terms, then this: you collect raspberries, make jam and sell them - you can work for the ESHN. You just buy raspberries and make jam out of them - you can’t work for the ESHN.

How to pay ESHN

The tax is calculated according to the following formula:

ESHN = Tax base × Tax rate

There is nothing complicated about tax calculation. It is difficult to determine what income and expenses can be taken into account. The tax code has a complete list of income and expenses. For example, the list of income includes income from the sale of goods, from the lease of land and interest on a bank deposit. The list of expenses includes the cost of salaries to employees, the payment of compensations and benefits, the purchase of seeds, seedlings, fertilizers, feed and medicine for animals, the maintenance of official vehicles.

Income can be reduced by the losses of previous years.

Tax rate. Previously, the rate was fixed, but since 2019, each region can set its own. Maximum - 6%.

In the Kemerovo region, entrepreneurs on the Unified Agricultural Tax pay a tax at a rate of 3% until 2021, in Moscow - at a rate of 6%, and in the Moscow region a zero rate. Entrepreneurs from the Moscow region do not need to pay tax - they only need to fill out a declaration.

When to pay

An accountant will help with the calculations, but here is a short example.

For the first six months, the entrepreneur earned - 600,000 R, expenses - 400,000 R. The tax rate is 6%.

(600,000 R − 400,000 R) × 6% = 12,000 R

In the second half of the year, the entrepreneur earned 800,000 R, expenses - 700,000 R. It is necessary to calculate the amount of ESHN for the whole year, and then subtract from it the already made advance payment.

Tax for the whole year:

(600,000 R + 800,000 R) − (400,000 R + 700,000 R) × 6% = 18,000 R

We deduct the advance payment:

18,000 R − 12,000 R = 6000 R.

In reality, the calculations are usually more complicated. You need to understand what expenses can be taken into account and which cannot. Therefore, I recommend that you seek the help of an experienced accountant.

VAT on ESHN

Since 2019, agricultural producers on the ESHN are required to pay VAT. But there are cases when a company or individual entrepreneur can be released from this obligation:

- If a company or individual entrepreneur has applied for a desire to take advantage of the benefit in the same year that they were registered.

- If you switched from DOS to UAT from January 1 and at the same time applied for VAT exemption.

- If the income from activities under the Unified Agricultural Tax for the previous year did not exceed the limit. It is different for every year. In 2018 - 100 million rubles, in 2019 - 90 million rubles, in 2020 - 80 million rubles.

In all cases, the notification is submitted to the tax office at the location of the company or at the place of residence of the individual entrepreneur. Deadline - until the 20th day of the month in which the benefit began to apply.

Accounting and reporting on ESHN

IP account. Entrepreneurs are not required to keep accounts. All reporting they have is a book of income and expenses and a tax return.

The book of income and expenses (KUDiR) can be kept online or in paper form. ESHN is the only mode in which you need to register a tax book: paper - before the start of maintenance, electronic print out and refer until March 31 of the next year.

The tax return must be submitted by March 31 of the year following the reporting year. For 2019, the declaration must be submitted by March 31, 2020.

If the agricultural producer stops working during the year, he must notify the tax authority and submit a declaration by the 25th day of the next month. For example, an entrepreneur stopped working in May and notified the tax office about this in the same month. The application must be submitted by June 25th.

Company accounting. For companies, everything is more complicated - they need to keep accounting: draw up a balance sheet and a statement of financial results, keep records of income and expenses that are involved in tax calculation. Tax returns are filed once a year, by March 31st.

Small agricultural companies, such as peasant and farm enterprises and consumer cooperatives, can keep accounting according to a simplified scheme. But you still need an accountant.

How to switch to ESHN

New sole proprietors and companies may submit a notification along with other registration documents or within 30 calendar days after registration. If you are late, you will have to work for the OSN and pay all taxes.

Combination of UAT with other tax regimes

Entrepreneurs can combine ESHN with a patent and UTII - a single tax on imputed income, and companies - only with UTII. True, there is a nuance: you cannot sell agricultural products through your own outlets and canteens. You cannot sell cucumbers from your garden in your vegetable stall, but a neighbor can buy them from you and sell them in his stall.

When combining regimes, the share of income from agricultural activities should be at least 70% of income for all types of business.

Deregistration of ESHN

A company or individual entrepreneur must be deregistered according to the Unified Agricultural Tax in three cases:

- If you have lost the right to work for the ESHN.

- If they no longer operate on the ESHN, for example, if the company has closed the agricultural line of business.

- If you want to switch to another system of taxation.

In any of these cases, you must submit a notice in two copies to the tax office at the location of the company or at the place of residence of the individual entrepreneur. You have 15 days from the date of the decision.

Loss of the right to ESHN

A company and an individual entrepreneur lose their right to the UAT if they no longer comply with the requirements of the legislation on this taxation system. For example, they began to produce excisable goods or the proceeds from agricultural activities fell below 70%.

If you have lost the right to ESHN, you must report this to the tax office. Then you will have to pay taxes, as if you have been working on a common system all year.

For example, for the first six months the company was engaged in the production and sale of honey. In the second half of the year, she changed her profile and began to produce mead - this is an excisable product. It is no longer possible to work for ESHN, so the company switched to DOS. She is required to pay DOS taxes for the entire year, even on income from the production and sale of honey.

-

April 17, 2015What should I do if I was denied an OSAGO?

April 17, 2015What should I do if I was denied an OSAGO? -

April 17, 2015New OSAGO tariffs: should we expect a rise in price?

April 17, 2015New OSAGO tariffs: should we expect a rise in price? -

April 17, 2015Is it possible to drive a car without a pts

April 17, 2015Is it possible to drive a car without a pts -

April 17, 2015What time and weather to pour the foundation

April 17, 2015What time and weather to pour the foundation